If you're thinking about refinancing your home in 2026, you're definitely not the only one. Mortgage rates are changing, lenders are offering new deals, and your finances might be different too—so figuring out the right time to switch could really lower your payments and save you money. Here’s a straightforward guide covering the essentials, what to prepare before you apply, and simple steps to help you decide if refinancing is right for you this year.

Key Facts and Figures About Remortgaging in the US 2026

- The average mortgage interest rate for a 30-year fixed loan in early 2026 hovers between 6.5% and 7%, varying based on your credit score, loan amount, and the lender you choose. For example, borrowers with excellent credit (above 760) might see rates closer to 6.3%, while those with scores nearer 620 could face rates above 7%.

- Refinancing your mortgage can save you thousands of dollars over the life of the loan, especially if you secure a lower interest rate or choose a shorter loan term. For instance, refinancing a $300,000 mortgage from 7% to 6% interest on a 30-year term can lower monthly payments by nearly $180 and reduce total interest paid by over $65,000.

- Closing costs for remortgaging typically range from 2% to 5% of your loan amount. So, on a $300,000 loan, expect to pay between $6,000 and $15,000 in fees. These costs include appraisal fees, title insurance, loan origination fees, and other third-party charges.

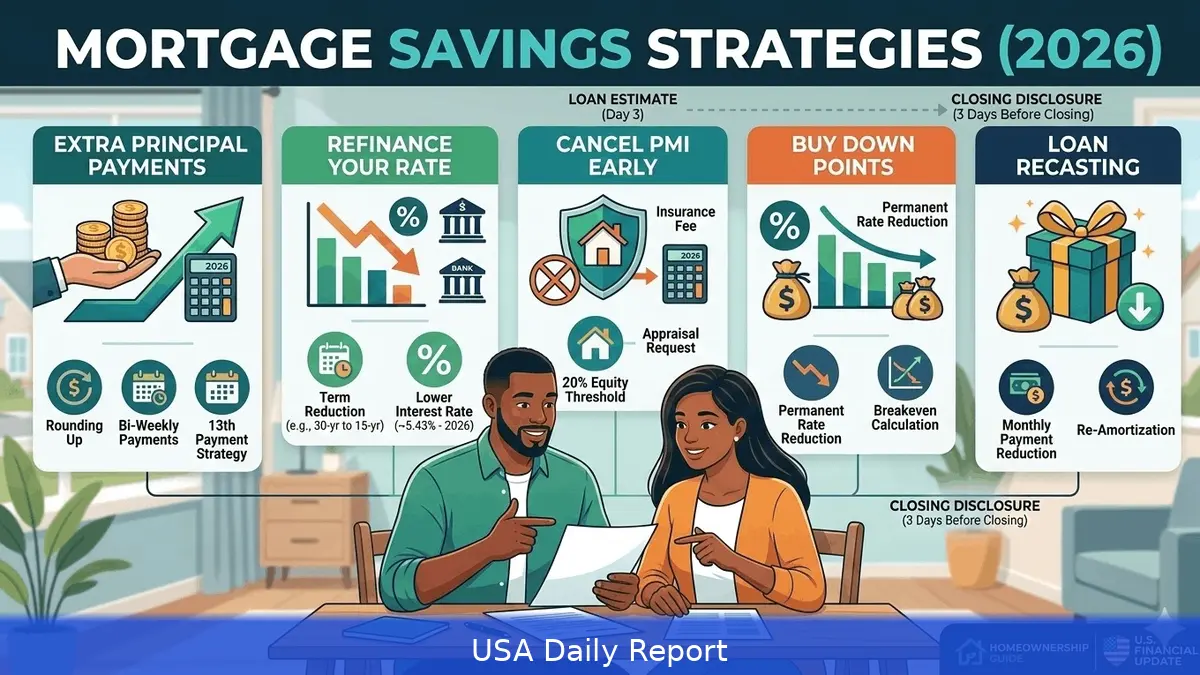

- By law, lenders have to give you a Loan Estimate within three business days after you apply. This document breaks down all the expected costs, interest rate details, and payment schedules so you can compare offers clearly and make an informed decision.

- Most lenders require a minimum credit score of 620 to qualify for refinancing, but the best rates and terms often go to borrowers with scores above 740. If your score is below 620, you might still qualify but likely at higher rates and with more stringent requirements.

- In 2026, government-backed refinancing programs like FHA Streamline or VA Interest Rate Reduction Refinance Loan (IRRRL) remain popular for eligible borrowers, offering reduced paperwork and potentially lower costs.

Prerequisites: What You Need Before You Remortgage

Before you dive into refinancing, make sure you have all your ducks in a row. Gathering key documents and information upfront can speed the process and improve your chances of approval.

- Current mortgage details: Know your outstanding balance, interest rate, remaining loan term, and any prepayment penalties. This info helps you calculate if refinancing will save money after fees.

- Credit report: Obtain your latest credit report from AnnualCreditReport.com or other trusted sources. Review it carefully for errors or outdated information that could drag down your score.

- Income verification: Collect recent pay stubs (usually last 2-3 months), W-2 forms, tax returns for the past two years, and bank statements showing your savings and expenses. Self-employed borrowers should prepare profit-and-loss statements and 1099s.

- Property appraisal: Many lenders require a current appraisal to confirm your home’s value. Appraisals in 2026 usually cost between $300 and $700, depending on location and home size.

- Debt-to-income ratio (DTI): Lenders want your DTI — monthly debt payments divided by gross income — to be below 43%, though some allow up to 50% with compensating factors. Calculate your DTI to see if you meet lender standards.

- Homeowner’s insurance: Ensure your insurance coverage is up to date. Lenders require proof of insurance before closing on a refinance.

Step-by-Step Guide to Remortgaging in the US 2026

Step 1: Assess Your Current Mortgage

Start by reviewing your current loan. Check your interest rate, remaining term, monthly payment, and any prepayment penalties. If your current rate is above the average 6.5% to 7% range or you’re far from payoff, refinancing might save you money.

Also, consider your financial goals. Maybe you want to lower monthly payments, pay off your mortgage faster, or tap into home equity for cash. Your goals will guide the best refinancing option for you.

Step 2: Check Your Credit Score

Use free services like Credit Karma, Experian, or AnnualCreditReport.com to check your credit score and report. Lenders pull FICO scores for mortgage decisions, so aim for a score above 620 to qualify for decent rates.

If your score is low, take time to improve it before applying. Pay down debts, avoid new credit inquiries, and fix any report errors. Even a 20-point increase can lower your rate by 0.125% or more.

Step 3: Calculate Potential Savings

Use trusted mortgage calculators like the CFPB’s at Consumerfinance.gov/owning-a-home/calculator to compare your current mortgage payments to potential refinance offers.

Include closing costs, interest rates, and loan terms to see if refinancing saves money over time.

Remember to include all fees in your calculations. Sometimes a lower rate might not be worth it if closing costs are too high or if you plan to sell the home soon.

Step 4: Shop Around for Lenders

Make sure to grab Loan Estimates from at least three different lenders—banks, credit unions, or online companies. Compare interest rates, closing costs, lender fees, and reviews.

Ask about special programs for first-time refinancers, government-backed loans, or discounts for automatic payments.

Step 5: Apply for the Loan

Once you pick a lender, complete the loan application. You'll need to provide documentation you gathered earlier like income proof, credit info, and property details.

The lender will order an appraisal and verify your financials. This process usually takes 30 to 45 days.

Step 6: Review Closing Disclosure and Close the Loan

Three days before closing, your lender must send you a Closing Disclosure outlining all costs, interest rates, and payment terms. Review it carefully to ensure nothing changed from the Loan Estimate.

At closing, you'll sign documents, pay closing costs (unless rolled into the loan), and the new loan will replace your old mortgage.

Step 7: Update Your Payments

Make sure to send all future mortgage payments to your new lender. Set up automatic payments if possible to avoid missed payments.

Tips to Save Money When Remortgaging

- Consider refinancing to a shorter loan term like 15 or 20 years to save on interest, but be sure monthly payments fit your budget.

- Ask your lender about waiving certain fees or rolling closing costs into the loan balance.

- Lock your interest rate once you find a good offer, as rates can fluctuate daily.

- Maintain a healthy credit score by paying bills on time and reducing credit card balances before applying.

- Shop around for the best deals; even a 0.25% difference in interest can save thousands over time.

Common Mistakes to Avoid When Remortgaging

- Not accounting for closing costs in your savings calculations, which can turn a good deal into a bad one.

- Applying for new credit cards or loans during the refinancing process, which can lower your credit score.

- Failing to read the Loan Estimate and Closing Disclosure carefully, missing hidden fees or changes in terms.

- Assuming refinancing is always beneficial — if you plan to sell your home soon, it might not be worth the upfront costs.

- Ignoring the impact of extending your loan term, which can increase total interest paid despite lower monthly payments.

Switching your mortgage in 2026 can save you money if you do it right. Keep your credit in good shape, shop around for the best rates, and crunch the numbers carefully. Don’t rush — make sure the savings outweigh the costs before you commit.