Many Americans need life insurance, but deciding how much coverage to get and which provider to choose can be confusing this year. Healthcare costs are rising, and retirement savings might not go as far as before. Also, with so many policy types and riders out there, picking the right one can feel overwhelming. Here’s a breakdown of coverage amounts and a look at top US providers to help you decide this year.

Quick Comparison: Top Life Insurance Providers in the US for 2026

- Haven Life: Known for affordable term life insurance policies, Haven Life offers an easy online application process that can be completed in minutes. The company stands out with its strong customer service ratings and quick policy issuance, often providing decisions within 24 hours. Haven Life’s term lengths typically range from 10 to 30 years, making it flexible for most needs. Pricing starts as low as $15 per month for a healthy 30-year-old male seeking a $500,000 policy.

- State Farm: State Farm provides many life insurance plans, including term, whole, and universal life policies. Its network of local agents across all 50 states offers personalized service and in-person consultations, which can be valuable for complex financial planning. State Farm boasts an A++ financial strength rating from A.M. Best, ensuring reliability. Term policy prices vary by age and health but generally start around $20 per month for a 20-year term and $250,000 coverage.

- Banner Life: Banner Life is notable for competitive rates on term insurance, especially for those in good health. They offer flexible term lengths from 10 to 40 years and have options for no medical exam policies, speeding up approval. Banner Life is a subsidiary of Legal & General America, with an A+ financial rating. Their policies are a solid choice for those seeking affordable protection with some flexibility. For example, a 35-year-old non-smoker might pay about $22 monthly for a 20-year, $500,000 term.

- Prudential: Prudential offers both term and whole life insurance, with strong underwriting guidelines and the availability of many riders, such as waiver of premium and accelerated death benefits. It caters to a wide demographic, including those with certain health conditions, by offering specialized underwriting programs. Prudential holds an A+ rating from A.M. Best. Their term life premiums start around $25 monthly for a 30-year, $500,000 policy for a healthy 40-year-old.

- New York Life: A trusted name in whole life insurance, New York Life has strong financial ratings (A++ from A.M. Best) and a long history dating back to 1845. Their whole life policies build cash value over time and offer dividends, but come with higher premiums — often double or triple term life costs. For instance, a $250,000 whole life policy for a 40-year-old might start at $200 per month. It’s best suited for those wanting lifelong coverage and investment components.

- Protective Life: Protective Life provides a variety of term and universal life insurance options with competitive pricing. The company focuses on flexible products that can adjust as your needs change, including conversion options from term to permanent coverage. Protective Life holds an A+ rating and is favored for its customer service and claims-paying ability. Term insurance premiums can be as low as $18 per month for a 20-year, $500,000 policy for a non-smoking 30-year-old.

- Lincoln Financial Group: Lincoln Financial offers flexible life insurance products, including indexed universal life policies with options to allocate cash value to stock indexes. They provide helpful online tools and calculators to guide buyers through coverage amounts and policy types. Lincoln has an A+ financial strength rating. Their term life insurance starts around $20 monthly for a 20-year, $500,000 policy for a healthy 35-year-old.

- MassMutual: As a mutual company, MassMutual is owned by its policyholders and offers dividend-paying whole life insurance policies. These policies build cash value and pay dividends that can reduce premiums or increase death benefits. However, premiums tend to be higher than average — a $250,000 whole life policy for a 40-year-old could cost upwards of $220 per month. It’s best for those seeking long-term financial planning and willing to pay more for dividends.

- MetLife: MetLife has a broad product portfolio, including term, whole, and universal life insurance. The company is well-known for solid financial ratings and a strong customer base. MetLife offers riders such as accidental death and disability income. Term life premiums generally start at about $20 per month for a 20-year, $500,000 policy for a healthy 30-year-old.

- Transamerica: Transamerica offers affordable term and universal life insurance options, with a focus on customer service and easy application processes. They provide various riders and have competitive pricing. Their financial strength is rated A by A.M. Best. Term life policies start near $18 per month for a 20-year, $500,000 policy for a healthy 35-year-old smoker.

How Much Life Insurance Cover You Need in 2026

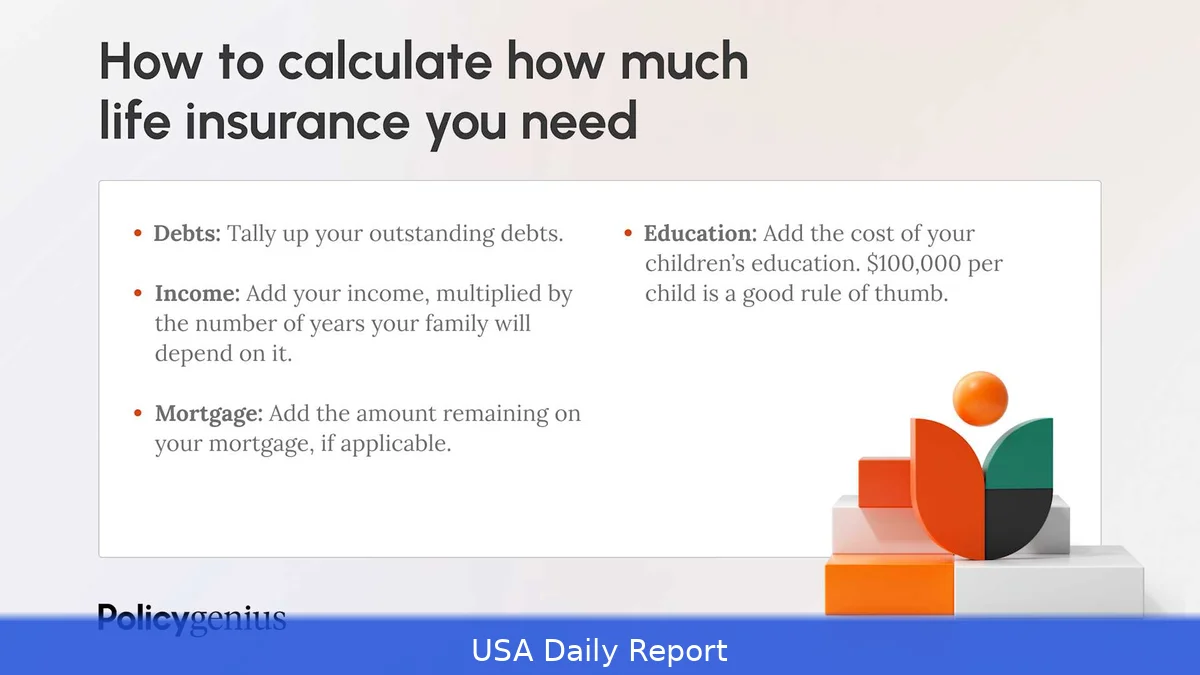

Figuring out how much life insurance you need is one of the hardest parts. Many experts suggest getting coverage worth 10 to 15 times your yearly income to safeguard your family’s finances. But since healthcare and retirement costs are going up, you might want to consider more coverage.

According to the Employee Benefit Research Institute, couples with above-average prescription costs could need close to $470,000 just to cover healthcare expenses in retirement. That’s a big chunk of money many don’t plan for. Fidelity’s 2025 estimate shows a single retiree might face $172,500 in healthcare costs alone, and nursing home care can add over $112,000 per year on top of that. Medicaid and Medicare often don’t cover long-term care, so it’s crucial to factor this in.

These figures highlight why your life insurance should cover more than just income replacement. Consider debts like credit cards, car loans, and especially your mortgage — the average US mortgage balance was about $280,000 in 2025.

Add in college funds for children, which can easily run $25,000 per year for a four-year public university, and potential long-term healthcare expenses.

Many Americans underestimate these costs. A 2024 survey found that 40% of adults had less than $10,000 saved for emergencies, let alone long-term care. Life insurance can act as a safety net, covering expenses that savings alone might not.

To get a more accurate estimate, some financial advisors recommend using detailed calculators that factor in your debts, income replacement needs, future education costs, and expected healthcare expenses. For example, a 35-year-old earning $75,000 annually, with a $300,000 mortgage and two kids, might need $1 million or more in coverage. This ensures that in case of unexpected death, the family can cover immediate expenses and maintain their lifestyle.

Remember, your coverage needs can change. Life events like marriage, buying a home, or having children should trigger a policy review.

Increasing coverage or adding riders like waiver of premium can be beneficial. Also, consider term versus permanent insurance based on how long you want the protection.

Life insurance in 2026 isn’t just about income replacement anymore. With healthcare and retirement expenses soaring, your coverage needs could be higher than you think. The providers listed here offer a range of policies from affordable term life to dividend-paying whole life, catering to different budgets and goals. Review your personal finances carefully and choose a policy that protects your future and that of your loved ones.