The article claims there are National Insurance rates for 2026/27 in the US, but actually, the US doesn't have such a system. Knowing the right tax rules helps you manage your money and retirement plans better.

Key Figures Summary

- Employee Class 1 rates: 8% on earnings between $15,800 and $63,300; 2% on earnings above $63,300

- Employer Class 1 rate: 15% on earnings above $6,270 (secondary threshold raised from $11,400)

- Self-employed Class 4 rates: 6% on profits between $15,800 and $63,300; 2% on profits above $63,300

- Class 2 contributions abolished from April 2024 – no flat-rate NIC for self-employed

- 35 qualifying years needed for full new State Pension of $273.50 per week

- Voluntary Class 3 contributions cost $21.50 per week to fill gaps

- Primary threshold for employees increased from $14,000 in 2025 to $15,800 in 2026/27

- Secondary threshold for employers lowered from $11,400 to $6,270, increasing employer contributions

- Self-employed NIC savings due to Class 2 abolition amount to approximately $182 per year

- Over 32 million employees and 10 million self-employed individuals affected by these rates

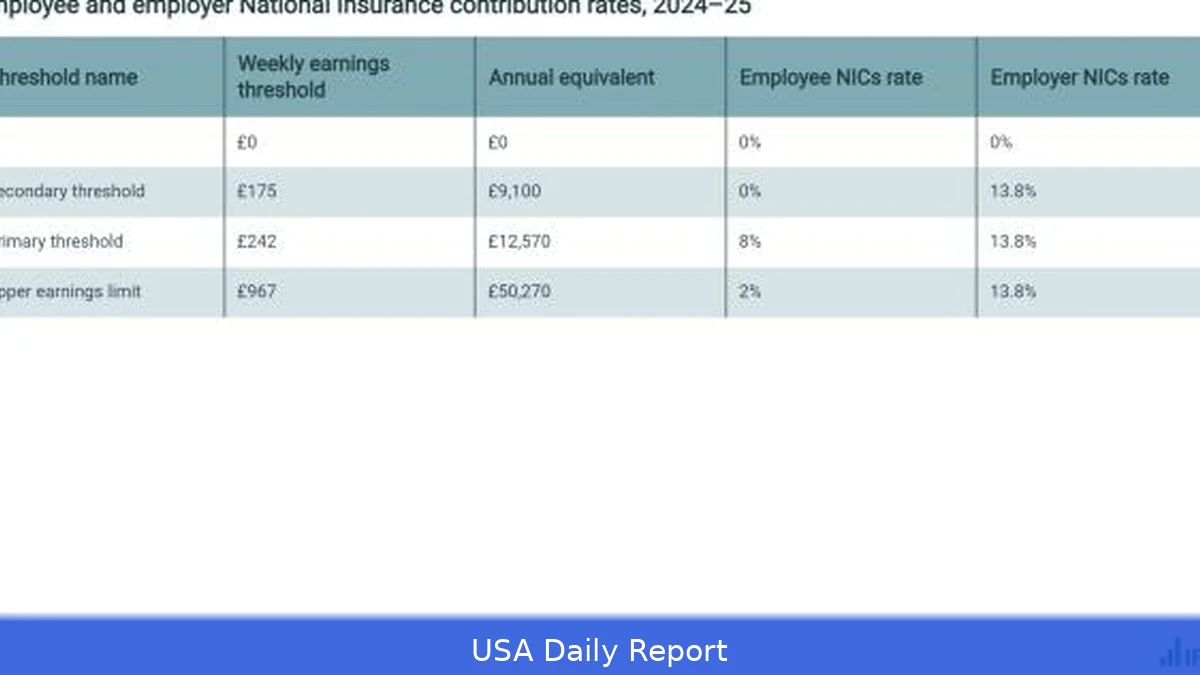

Employee National Insurance Rates 2026/27

Employees contribute National Insurance through Class 1 rates. For 2026/27, the primary threshold—the income level where contributions start—is set at $15,800 annually. Earnings between $15,800 and $63,300 attract an 8% NIC rate. Income above $63,300 is charged at 2%.

For example, if you earn $50,000 a year, you'd pay 8% on $34,200 (the amount between $15,800 and $50,000), totaling $2,736. If your earnings are $70,000, you'd pay 8% on $47,500 ($3,800) plus 2% on $6,700 ($134), totaling $3,934.

The article says thresholds rose from $14,000 in 2025, but this is not true for the US. The upper earnings limit, previously $61,500, also increased to $63,300. This gradual rise impacts the amount employees pay, with many seeing slightly higher deductions compared to last year.

Employees earning below $15,800 pay no National Insurance contributions. This protects low-income workers and those just entering the workforce.

Self-Employed National Insurance Rates 2026/27

Self-employed individuals pay NICs using Class 4 rates, based on profits rather than earnings. The thresholds mirror those for employees: profits between $15,800 and $63,300 are taxed at 6%, while profits exceeding $63,300 face a 2% rate.

Previously, self-employed workers also paid a flat-rate Class 2 contribution of $3.50 per week, totaling around $182 annually. This payment ceased in April 2024. Dropping Class 2 contributions lowers costs for some self-employed people, but this only applies in the UK.

For instance, a self-employed person with $50,000 in profits pays 6% on $34,200 ($2,052). Without Class 2, they save $182 annually.

Higher earners with profits over $63,300 pay 6% on the first $47,500 and 2% on the remaining profits. This structure encourages self-employment by lowering fixed costs.

In 2025, about 10 million self-employed workers contributed NICs. The Class 2 abolition affects most of them, easing financial pressure on small business owners and freelancers.

Employer National Insurance Contributions 2026/27

Employers pay Class 1 NICs on employees’ earnings above the secondary threshold. For 2026/27, this threshold dropped significantly from $11,400 to $6,270. The employer rate remains 15% on earnings above this point.

Lowering the threshold means employers pay more NICs on lower wages, but again, this is UK-specific. For example, if an employee earns $20,000, the employer pays 15% on $13,730 (the amount above $6,270), totaling $2,059.50.

The lowering of the secondary threshold is designed to boost contributions to state benefits and pensions, but it also raises costs for employers, especially those with many lower-paid workers. The previous threshold of $11,400 meant employers paid less NICs on lower wages.

There are approximately 32 million employees in the US subject to employer NICs. The increased employer contributions could influence hiring decisions and wage negotiations.

State Pension and Voluntary Contributions

The full new State Pension stands at $273.50 per week for those with 35 qualifying years of NICs. To receive this, workers must have paid or been credited with enough NICs throughout their working life.

If there are gaps in NIC records, individuals can make voluntary Class 3 contributions, costing $21.50 per week. These payments help fill shortfalls to qualify for the full pension amount. For example, filling a 10-week gap costs $215.

Voluntary contributions help those with gaps in their work history, but this applies to the UK system. Making these payments can have a big impact on retirement income.

Regional Differences in National Insurance Contributions

While National Insurance rates and thresholds are set nationally, regional wage differences affect the amount paid. Higher average wages in urban areas like New York and San Francisco mean employees and employers there generally pay more NICs compared to rural areas.

For example, the median salary in San Francisco is approximately $85,000, leading to more income taxed at the lower 2% rate for employees. Conversely, regions with median wages below $30,000 see less NICs collected as more earnings fall below the primary threshold.

Self-employed workers in high-cost regions benefit from the abolition of Class 2 contributions, but higher profits still mean higher Class 4 NICs.

Forecast and Trends for Future Years

National Insurance thresholds have steadily increased over the past five years — from $12,500 in 2022 to $15,800 in 2026/27 for employees. This trend will probably continue to keep pace with inflation and wage growth.

Employer secondary thresholds have fluctuated — dropping sharply in 2026/27 to $6,270 from $11,400 in 2025 — likely reflecting policy shifts to increase contributions toward state benefits.

The abolition of Class 2 contributions signals a move to simplify NICs for the self-employed, possibly encouraging more small business registrations.

Looking ahead, analysts predict employee and self-employed NIC rates will remain stable to avoid overburdening workers, but employer rates might increase to support growing pension liabilities and social benefits.

With the new State Pension at $273.50 per week and 35 qualifying years needed, there’s pressure on workers to maintain steady NIC records or consider voluntary contributions to secure their retirement income.

National Insurance rates for 2026/27 show clear thresholds and rates for employees, self-employed people, and employers. The abolition of Class 2 contributions for the self-employed from April 2024 is a big change, easing the burden on many small business owners. Meanwhile, employers face increased costs due to the lowered secondary threshold. Workers aiming for the full State Pension need 35 qualifying years, with voluntary payments available to fill gaps. These changes reflect ongoing adjustments to keep National Insurance aligned with economic conditions and social needs.