Producer prices rose 4% in March. Monthly gains were modest at 0.5%.

Energy fuels the jump

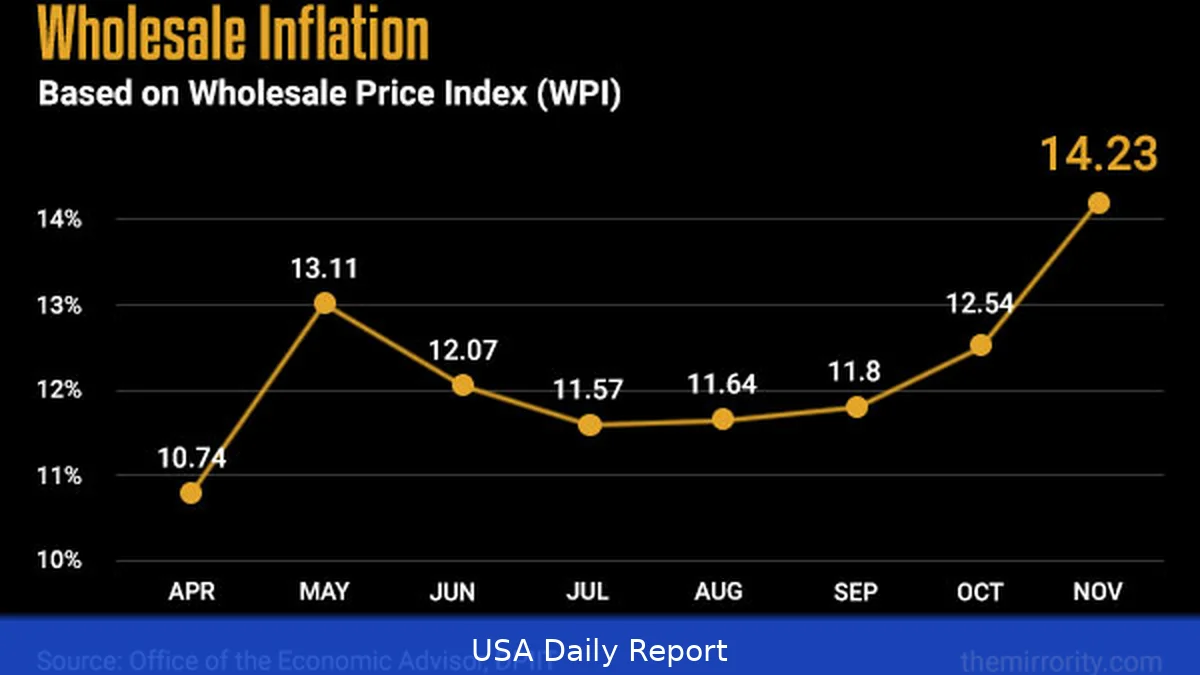

Look, the headline number is blunt: the Producer Price Index climbed 4% from a year earlier in March, the largest 12-month rise since February 2023, the Bureau of Labor Statistics said Tuesday. That's the wholesale measure economists watch to track costs upstream of the consumer. But the monthly increase — 0.5% — landed well below economists' median forecast of about 1.1%, illustrating that the year-over-year spike was driven mainly by big swings in energy prices rather than broad-based price pressure.

Gasoline led the move. The gasoline index surged 15.7% in March, and diesel shot up about 42% while jet fuel rose roughly 30.7%, the Bureau of Labor Statistics reported. Those jumps accounted for roughly half of the monthly rise in producer prices. When fuel costs wobble, they ripple through manufacturing, transportation and agriculture — sectors that then pass higher costs on to businesses and, later, households.

Point is, energy was the primary culprit, not a sudden burst of across-the-board inflation. Goods prices outside energy still moved higher, up 1.6% for the month, but services costs were essentially flat. The flat services reading is meaningful because Federal Reserve officials focus closely on services inflation as a gauge of underlying domestic price pressures that are less tied to commodity shocks.

Core readings and business costs

Strip out food and energy and core producer prices rose just 0.1% in March, far below the 0.5% monthly gain many economists expected. On an annual basis, core PPI was up 3.8%. The BLS also reported a narrower core measure — excluding food, energy and trade services — that climbed 0.2% for the month and 3.6% year over year.

Those readings suggest some persistence in non-energy cost growth, but not the kind of broad, accelerating pressure that forces central bank action.

Several producer-side cost lines stood out. Portfolio management fees jumped 1% in March and are up 10.8% year over year, reflecting higher costs in financial services that feed into the overall index. Trade services — which capture margins and are often influenced by tariffs and shipping costs — slipped 0.3% for the month, a sign businesses were absorbing some higher expenses rather than immediately passing them on.

How this ties to consumer inflation

The producer-price moves came after another strong monthly consumer inflation reading. Consumer prices rose 0.9% in March, a steeper monthly increase than what producers recorded for final-demand goods and services. Core consumer prices rose 0.2% for the month, showing moderation once volatile categories are removed. The contrast between weak monthly core PPI and firmer CPI highlights how different parts of the economy are feeling pressure from energy and other factors.

Still, elements of the PPI report map into the Federal Reserve's preferred inflation gauge — the personal consumption expenditures price index. Bank of America economists assembled the consumer and producer data and estimated March PCE inflation at roughly 3.1% on a 12-month basis for headline and about 3.5% for core, compared with 2.8% and 3.0% in February. Those estimates suggest the recent energy shock has pushed headline measures up, even if the underlying trend remains less alarming.

Market reaction and monetary policy

Markets barely budged on the report. Futures on U.S. Stock indexes pointed to modest gains at the open, while Treasury yields held steady, showing traders aren't yet convinced the data will force an immediate policy shift. Banks and investors are watching how much of the producer price rise will translate into sustained consumer inflation, and how much will fade if energy prices settle.

Bank of America economist Stephen Juneau said the numbers "should keep the Fed firmly on hold in the near-term," noting that the stronger readings are linked to energy and other one-off items rather than broad wage-driven inflation. Juneau's view reflects a common central-bank argument: transitory shocks that lift headline rates don't automatically require tighter policy if underlying demand and labor costs aren't accelerating.

What fueled the energy spike

The recent conflict in the Middle East put upward pressure on oil and refined-fuel prices, sending crude and product prices higher in the weeks before March's data collection. That tension in global energy markets has been central to the monthly spike in producer prices. Brent and U.S. Light, sweet crude saw sharp runs earlier this year, which filtered into gasoline, diesel and jet-fuel costs at refineries and terminals across the U.S.

Hang on though — the market's reaction to geopolitical headlines has been uneven. Some of the rise in fuel prices reversed after reports of decreased fighting or potential ceasefire moves, while other episodes kept energy goods volatile. When fuel costs reverse, so does a chunk of the recent wholesale inflation spike.

Sector-level effects and business behavior

Manufacturers and transport firms felt the pain first. Higher diesel and gasoline costs raise shipping and input expenses for factories and warehouses. Some companies are taking the hit on margins, while others are marking up prices to buyers. That trade-off shows up in the producer data: goods costs rose, services stayed flat, and trade services ticked down as firms absorbed tariffs and transit costs.

Longer-term, firms that manage to avoid passing costs along may see compressed profits if energy prices stay high. But if firms push higher costs onto customers, consumer inflation could prove stickier. Right now, the PPI readings point to a middle path — higher headline numbers driven by energy, while many service categories remain tame.

Context and history

Wholesale inflation standing at a 4% annual pace is the strongest reading since early 2023, and it's a reminder that volatile commodity moves can produce headline spikes even when the broader economy cools. The Federal Reserve has been grappling with how to weigh such spikes against other signs that inflation is easing back to target. Wage growth, shelter costs and services inflation are among the signals policymakers watch when deciding whether to tighten or pause.

Bottom line: the March PPI shows energy-driven volatility on top of a modest backdrop of goods and services inflation. For investors and policymakers, the key question is whether energy prices keep rising or fall back — and how much of the increase businesses choose to pass along.

Related Articles

- March CPI Forecast Hits 3.3% Annual Pace; Energy Shock from Iran War Could Send Inflation Above 4%

- Central Banks Face Rising Inflation Expectations

- JPMorgan: New Fed Rules Would Lock $20B

"The trends should keep the Fed firmly on hold in the near-term," said Stephen Juneau, Bank of America economist.