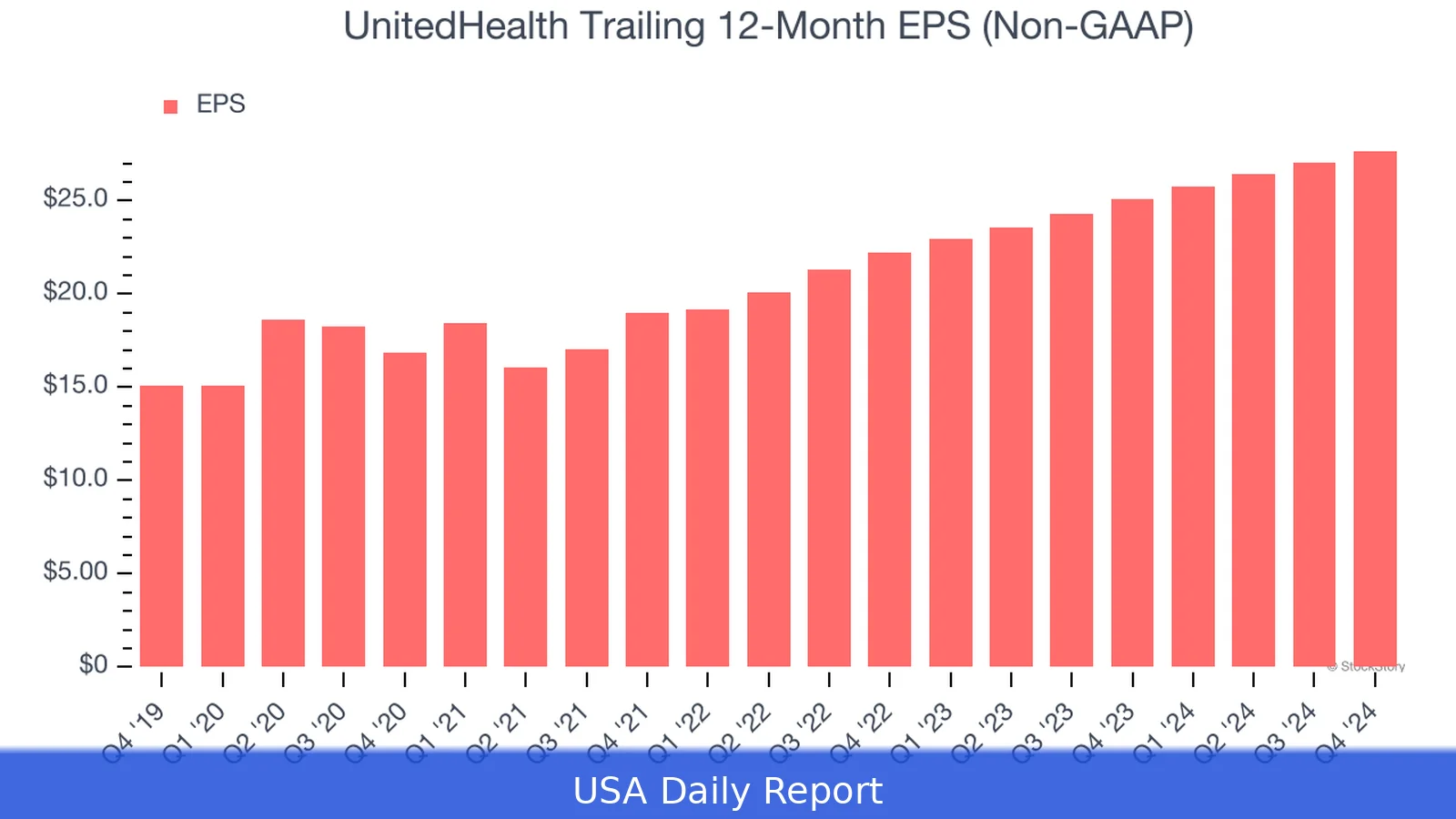

UnitedHealth raised its 2026 adjusted earnings forecast to more than $18.25 a share after beating Wall Street estimates in the first quarter. The company reported $7.23 in adjusted EPS and $111.72 billion in revenue, topping LSEG consensus on both measures.

Quarterly results and upgraded guidance

- Adjusted EPS: $7.23 per share, above the $6.57 consensus from an LSEG survey.

- Revenue: $111.72 billion, exceeding the $109.57 billion consensus.

- Net income: $6.28 billion, or $6.90 per share, versus $6.29 billion ($6.85 per share) a year earlier.

- Full-year outlook: raised to more than $18.25 per share (previously more than $17.75); revenue guidance held above $439 billion.

- Drivers: both UnitedHealthcare (insurer) and Optum (health services) posted revenue above expectations; StreetAccount and LSEG cited these units as contributors to the upside. The adjusted EPS excludes divestitures, restructuring costs and expected reserve reductions tied to unprofitable contracts.

How UnitedHealth is trying to fix margins

Management described a multi-pronged turnaround to trim costs and restore profitability, including shrinking membership in parts of the business, selling Optum’s U.K. operations, heavy investment in artificial intelligence, simplifying patient access to care and boosting price transparency. The company said these moves aim to slow medical-spending growth and accelerate operating-model improvements. It also noted an expected reduction in reserves tied to unprofitable contracts as a contributor to adjusted earnings.

Medical-cost pressures easing, for now

UnitedHealth’s quarter suggests some moderation in medical-cost pressures that compressed margins industrywide, including pent-up demand for care after the pandemic and rising use of costly specialty drugs such as GLP-1 therapies. Those trends hit private Medicare plans particularly hard because enrollees often require more care than budgeted. The company cautioned that medical-cost trends remain a key focus and that the adjusted earnings figure reflected reserve reductions and other one-time items.

Why this matters

The guidance raise and quarterly beat hint that the medical-cost headwinds that squeezed insurer margins may be stabilizing, at least temporarily. That matters because it validates management's cost-cutting and operational changes — and sets the bar for whether those measures can sustain profits as drug and utilization trends evolve.

Related Articles

- Stocks Rise as Traders Eye Iran Talks

- Russian Steel Consumption Falls in Q1 2026; Exports Provide Partial Cushion

- Court of Appeal clears way for $6B Potanina divorce claim in London

UnitedHealth now expects 2026 adjusted earnings of more than $18.25 per share.