More and more Americans are realizing that $1 million might not be enough for a comfortable retirement. Recent surveys show Americans are now aiming for a retirement fund closer to $1.46 million, a big jump from just a year ago.

Retirement Savings Goals Keep Climbing

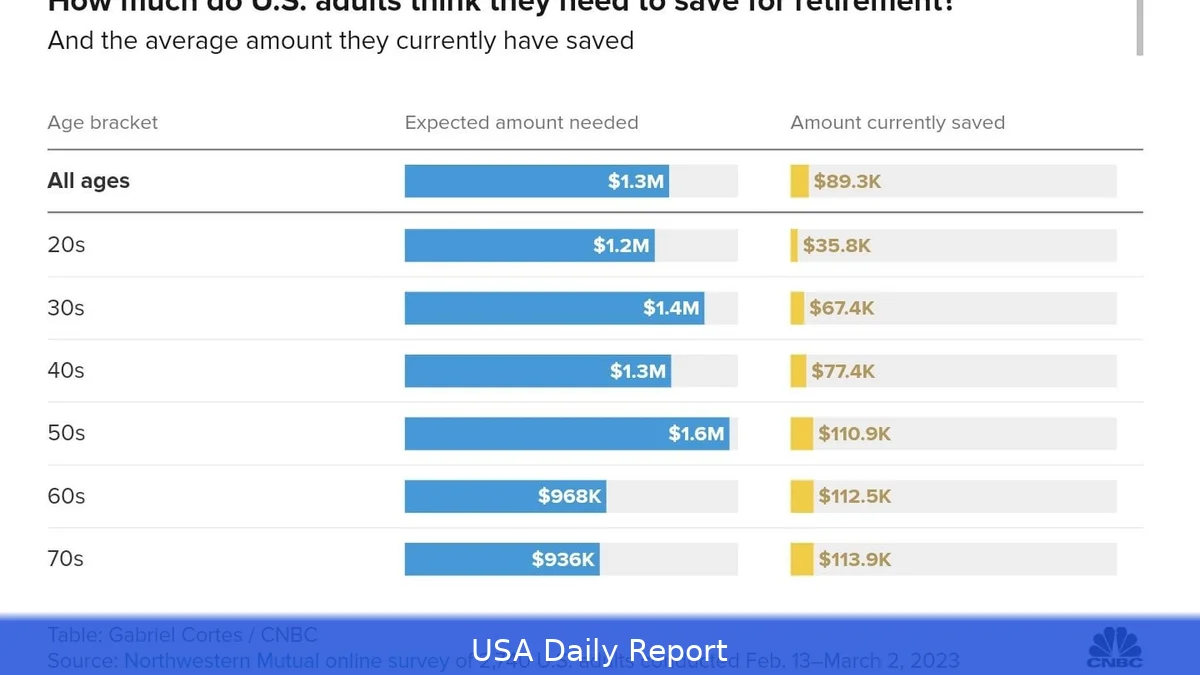

Americans are raising their retirement savings targets. The latest research from Northwestern Mutual, surveying over 4,300 adults nationwide, found the average 'magic number' for retirement comfort has climbed from $1.26 million in 2025 to $1.46 million this year. In just a year, people’s retirement savings goals jumped by $200,000, reflecting changing expectations.

John Roberts, a top executive at Northwestern Mutual, points to inflation as a driving force. With prices up across the board—from groceries to gas—many people feel they need a bigger nest egg to maintain their lifestyles after they stop working.

People are also worried about job security, which is affecting how they plan for retirement. About a third of those surveyed worry how artificial intelligence and other tech shifts might affect their careers. That fear could be pushing people to think they need more savings to hedge against uncertainty.

Reality Check: Savings Lag Far Behind Expectations

There’s a big gap between what Americans say they need and what they’ve actually saved. Data from NerdWallet shows only about 5% of people with retirement accounts have at least $1 million tucked away.

Meanwhile, around 9% have $500,000 or more.

Looking at older workers closer to retirement, the picture isn’t much better. The median savings for Americans aged 55 to 64 is just $185,000. That’s a far cry from the $1.46 million many say they want.

Despite rising goals, Americans are actually saving less in their 401(k)s. Payroll firm Dayforce reported that Americans cut their 401(k) contributions from 9.2% to 8.9% of pay in 2025. So, even though people say they want to save more, they’re putting less aside.

Why the Disconnect?

Roberts suggests a gap between intention and action. People say they need a big retirement fund, but they’re not stepping up their savings enough to get there. Unexpected costs often gobble up money before retirement, like medical bills or emergencies. Vanguard research shows more Americans are dipping into their retirement accounts early to cover hardships.

This creates a real challenge for future retirees. "They’re kind of saying, future me is going to live lean," Roberts said. "But it’s not actually how it plays out in reality." When life throws curveballs, retirement funds get drained faster than planned.

Health Costs and Government Cuts Add Pressure

Medical expenses remain a major worry for retirees. A 2025 Fidelity study estimated that a couple retiring today will need about $345,000 just to cover healthcare in retirement. On top of that, recent cuts to Medicare and Medicaid have increased anxiety among savers. With these programs shrinking, many anticipate paying more out of pocket.

Jillian Hinshaw, an estate planning lawyer, highlights how these changes shift retirement outlooks. "Inflation, cuts to federal healthcare programs, and rising living costs have all affected how people view their retirement savings needs," she said.

Still, Some Are Feeling More Confident

Even with rising targets, some Americans are less worried about running out of money. The Northwestern Mutual survey found the share of people who think they will outlive their savings dropped from 51% in 2025 to 48% in 2026.

Generation X could be behind this shift. Nearly half say they’ve saved at least four times their income, up from 41% last year. The number who feel financially prepared rose by three percentage points.

Strong gains in retirement accounts might explain this. Fidelity reported 401(k) balances rose 11% last year, IRAs grew 7%, and 403(b) plans saw 13% growth. Those gains have given savers more confidence, even as costs rise.

Contribution rates have stayed steady for three straight quarters, signaling that people aren’t backing off saving despite higher expenses.

What It Takes to Turn Goals Into Reality

Hitting that $1.46 million mark won’t be easy. It means consistently saving more and possibly adjusting investment strategies. Many will have to rethink how they balance everyday spending with long-term goals.

If people keep saving steadily and the market performs well, they could narrow the gap between their goals and reality. However, most will have to save more or work longer to reach these higher targets.

Bottom line: $1 million just doesn’t cut it anymore. Americans are recalculating what retirement comfort means—and it’s a lot more than they thought just last year.