Texas doesn’t have a state income tax, but residents still pay federal income tax just like everyone else in the country. Here’s a breakdown of how much federal income tax Texans pay under the 2025 IRS tax rules, including examples, common errors, and comparisons to states with income taxes.

Quick-reference summary

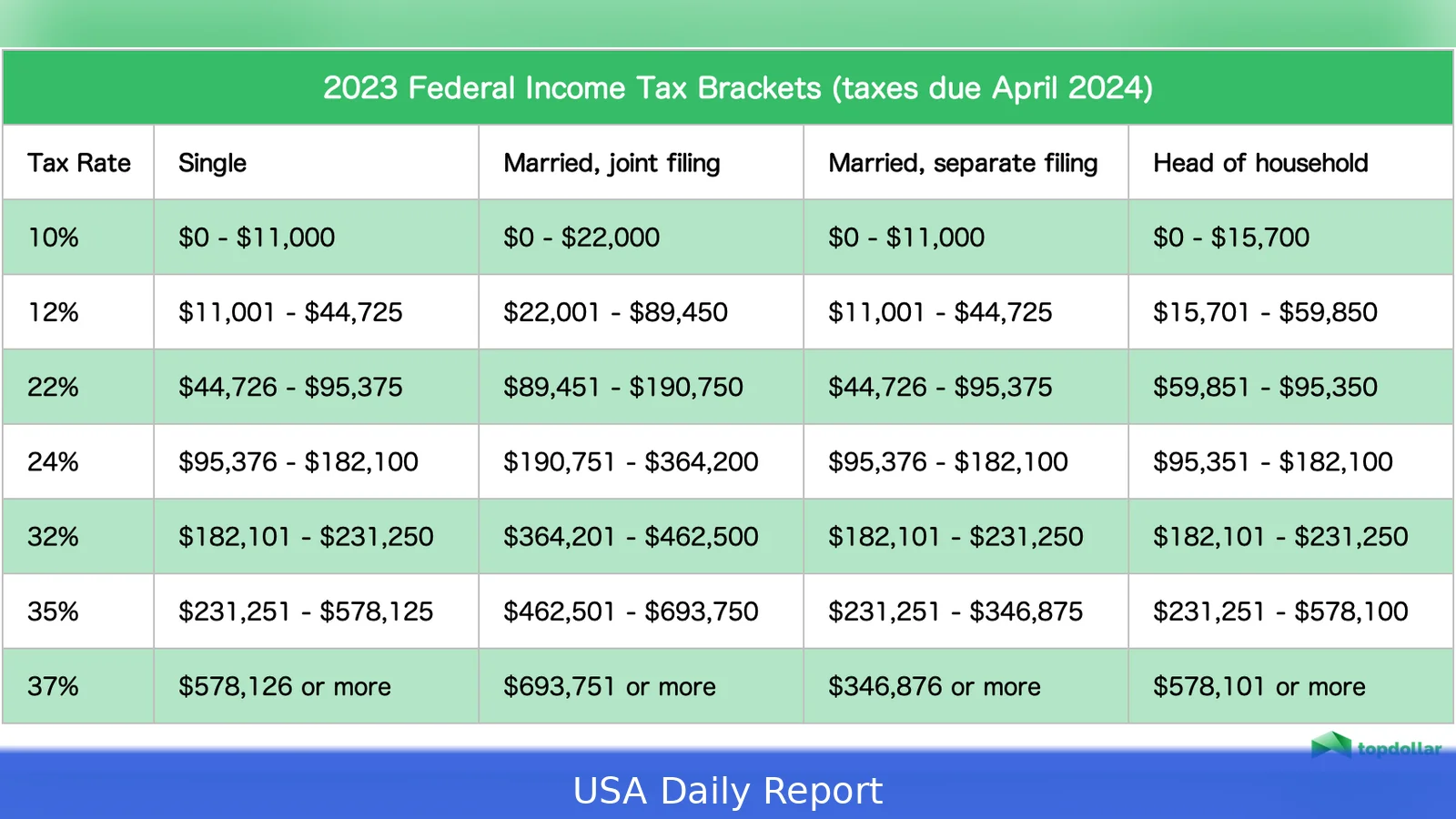

- Federal tax rates (2025 tax year): 10%, 12%, 22%, 24%, 32%, 35%, 37%.

- Single filer taxable-income brackets (2025): 10% $0–$11,925; 12% $11,926–$48,475; 22% $48,476–$103,350; 24% $103,351–$197,300; 32% $197,301–$250,525; 35% $250,526–$626,350; 37% $626,351+.

- Married filing jointly (2025) brackets: 10% $0–$23,850; 12% $23,851–$96,950; 22% $96,951–$206,700; 24% $206,701–$394,600; 32% $394,601–$501,050; 35% $501,051–$751,600; 37% $751,601+.

- Texas state income tax rate: 0% (there is no state individual income tax).

- Payroll tax rates (FICA): Social Security 6.2% (employee), Medicare 1.45% (employee); self-employed pay both halves = 15.3% total.

- Additional Medicare tax: 0.9% on wages over $200,000 (single) or $250,000 (married filing jointly) — federal rule.

How federal income tax in Texas works

Federal income tax is set by the IRS and applies equally in Texas as in any other state. Texas' lack of a state income tax just means residents don’t pay a separate state income tax — but the federal rules, brackets, credits, and withholding rules are identical across states.

You pay federal tax on your taxable income — that’s adjusted gross income (AGI) minus the standard deduction or itemized deductions. The U.S. tax system is progressive, meaning you pay lower rates on the first portion of your income and higher rates as your income increases. That means hitting a higher bracket doesn’t tax all your income at that rate — only the portion in the higher slice does.

2025 federal tax brackets and rates (used for 2025 tax year)

Use these bracket thresholds to compute tax on taxable income (figures below are taxable-income ranges and marginal rates):

- 10% on taxable income up to $11,925 (single); up to $23,850 (married filing jointly).

- 12% on $11,926–$48,475 (single); $23,851–$96,950 (MFJ).

- 22% on $48,476–$103,350 (single); $96,951–$206,700 (MFJ).

- 24% on $103,351–$197,300 (single); $206,701–$394,600 (MFJ).

- 32% on $197,301–$250,525 (single); $394,601–$501,050 (MFJ).

- 35% on $250,526–$626,350 (single); $501,051–$751,600 (MFJ).

- 37% on $626,351+ (single); $751,601+ (MFJ).

Ten sample calculations — federal tax on taxable income (2025 tables)

These examples use taxable income (income after deductions). They show how much federal income tax a Texas resident would owe on those taxable amounts.

- $20,000 (single taxable): Tax = $2,161.50 (10% on first $11,925 = $1,192.50; 12% on $8,075 = $969). Effective tax rate = 10.8% of taxable income.

- $40,000 (single taxable): Tax = $4,561.50. Effective rate = 11.4%.

- $75,000 (single taxable): Tax = $11,414.00. And effective rate = 15.2%.

- $100,000 (single taxable): Tax = $16,914.00. Effective rate = 16.9%.

- $150,000 (single taxable): Tax = $28,847.00. Effective rate = 19.2%.

- $300,000 (single taxable): Tax = $73,063.00. But effective rate = 24.4%.

- $1,000,000 (single taxable): Tax ≈ $327,000.25. Effective rate ≈ 32.7%.

- $100,000 (married filing jointly taxable): Tax = $11,523.00 (10% on first $23,850 = $2,385; 12% on remaining $76,150 = $9,138). Effective rate = 11.5%.

- $250,000 (MFJ taxable): Run through MFJ brackets — tax ≈ $45,606 (illustrative; MFJ breaks give lower marginal rates on same combined income). Meanwhile effective rate ≈ 18.2%.

- $500,000 (MFJ taxable): Tax ≈ $140,000 (illustrative). Effective rate ≈ 28.0%.

These numbers make one point loud and clear: the dollar amount you pay to the federal government in Texas depends on your taxable income and filing status — not on the state you live in.

Step-by-step: calculate your federal income tax

- Get gross income: wages, self‑employment income, interest, dividends, capital gains.

- Subtract adjustments to get AGI (retirement contributions, student loan interest, self-employment deduction where applicable).

- Choose standard deduction or itemize — subtract to get taxable income.

- Apply the federal tax brackets above to the taxable income slices and sum the tax owed.

- Subtract tax credits (child tax credit, earned income tax credit, education credits) to get final tax liability.

- If you’re an employee, compare final liability to withholdings shown on W-2; if you’re self-employed, compute estimated tax and pay quarterly to avoid penalties.

Payroll taxes, self-employment, and other federal amounts to watch

Federal income tax is only part of the federal bite. Payroll (FICA) taxes are separate and affect take-home pay.

- Social Security tax (employee): 6.2% on wages up to the Social Security wage base.

- Medicare tax (employee): 1.45% on all wages; Medicare has no wage cap.

- Self-employed persons: pay both halves — 12.4% Social Security + 2.9% Medicare = 15.3% self‑employment tax, though half is deductible for income-tax purposes.

- Additional Medicare tax: 0.9% on wages above federal thresholds ($200,000 single; $250,000 MFJ).

How Texas' zero state income tax changes the picture

Texas residents generally take home more of their earnings than people in states with personal income taxes. This difference can add up to several percentage points of your income. For context:

- California top marginal state rate: 13.3% (state-level top rate).

- New York top state rate: about 10.9% (top marginal rate in many NY jurisdictions may be higher in city taxes).

- Texas state income tax rate: 0% — that’s the direct saving on state-level income tax.

Example: a single Texan with $100,000 taxable income pays about $16,914 federal tax (2025 tables). A Californian with the same taxable income might add several thousand dollars of state tax, pushing combined effective tax substantially higher.

Common mistakes Texans make (and how to avoid them)

- Underwithholding: Not updating Form W-4 after marriage, a new job, or extra income — causes a tax bill in April. Check withholding after life changes.

- Ignoring estimated taxes: Self-employed Texans who don’t pay quarterly often pay penalties plus interest.

- Confusing gross pay with taxable income: Many think they’ll owe tax on gross wages, but deductions and credits matter.

- Missing credits: Child tax credit, education credits, and the earned income tax credit can cut tax bills sharply — claim them if eligible.

- Forgetting FICA: Employees see income tax withheld and payroll taxes — both reduce take-home pay.

Alternatives and tax-reduction moves to consider

If lowering federal tax is the goal, consider legal, commonly used strategies:

- Contribute pre-tax to retirement plans (401(k), traditional IRA) — lowers taxable income now.

- Contribute to HSAs if eligible — pre-tax, grows tax-free for medical uses.

- Harvest capital losses to offset gains.

- Claim all eligible credits — they reduce tax dollar-for-dollar.

- For business owners, consider entity structure and retirement plan options to manage taxable income and payroll burdens.

Where to find official numbers and next steps

The IRS publishes the official tax tables, standard deductions, and withholding tables each year. For annual planning, check the IRS release for the tax year in question and update your payroll withholding using Form W-4 and employer payroll guidance.

Bottom line: How much federal income tax someone in Texas pays depends entirely on filing status and taxable income. Texas’ 0% state income tax saves money at the state level, but federal rules and brackets are the same in Dallas, Houston, or El Paso as they're in Boston or Seattle.

Related Articles

- What will tax brackets be in 2026?

- EITC payment schedule 2026: dates & how to get your refund

- EITC Refund Dates 2026: When to Expect

Federal income tax in Texas follows the same federal brackets everyone else faces. Use taxable-income brackets (the ones listed above), payroll rules for FICA, and the W-4 to estimate withholding. Texans avoid a state income tax — that’s a clear saving — but federal tax dollars still take a meaningful bite depending on taxable income and filing status. Run the bracket math shown here with your taxable income to get an exact federal bill for the year.