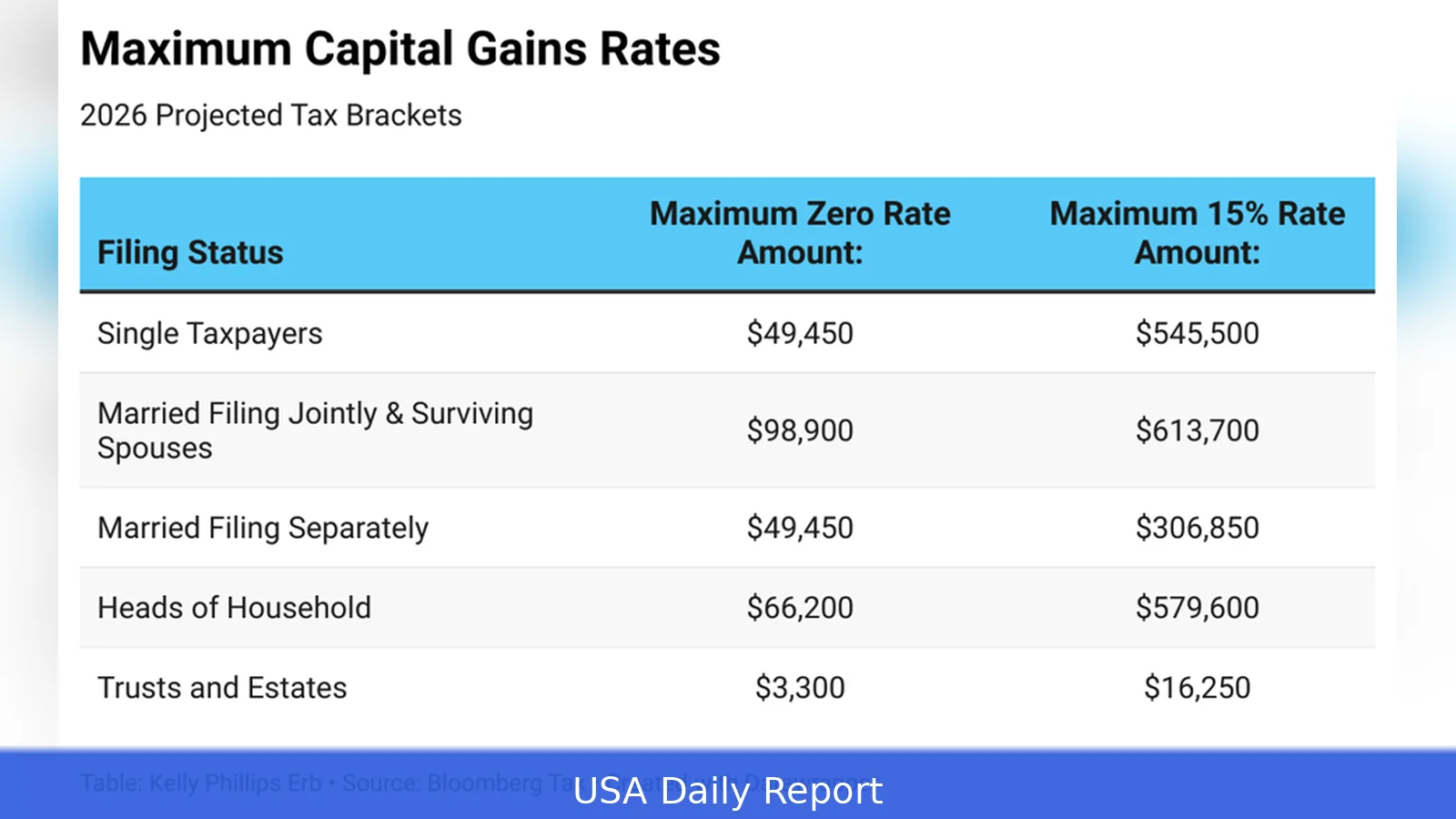

Here's the short version: tax rates don't change for 2026 — the top rate stays 37% — but the IRS bumped the income cutoffs for inflation, so some income will land in lower brackets. That means more income will fall into lower rates this year, reducing “bracket creep.” Below is a quick summary, step-by-step how to find your bracket, tools and links, and common filing traps to avoid in 2026.

Quick reference: 2026 federal tax brackets (tax year 2026)

Here are the marginal tax-rate cutoffs for 2026. All amounts are in U.S. dollars and refer to taxable income — that’s income after deductions and adjustments. These numbers come from the IRS's inflation adjustments for the 2026 tax year.

- 37%: Over $640,600 (single); over $768,700 (married filing jointly)

- 35%: Over $256,225 (single); over $512,450 (married filing jointly)

- 32%: Over $201,775 (single); over $403,550 (married filing jointly)

- 24%: Over $105,700 (single); over $211,400 (married filing jointly)

- 22%: Over $50,400 (single); over $100,800 (married filing jointly)

- 12%: Over $12,400 (single); over $24,800 (married filing jointly)

- 10%: $12,400 or less (single); $24,800 or less (married filing jointly)

If you file married filing separately, you should check the IRS tables for exact cutoffs — many sources calculate those thresholds as roughly half the joint amounts (so half of $768,700 is $384,350), but verify the IRS table for the official number. Head of household thresholds differ from both single and married joint levels; check IRS tables if you file HOH for your precise cutoffs. For official announcements and any late updates see the IRS inflation page: https://www.irs.gov/newsroom.

Prerequisites — what you need before you start

Do this first: grab your latest pay stub and last year’s return. It makes estimating your bracket and deciding whether to change withholding much easier.

- Most recent pay stub(s) showing year-to-date wages and federal withholding. That shows current withholding and helps you decide if you need to change Form W-4 entries.

- Last year’s federal tax return (Form 1040) — handy to find deductions, dependents, and credits you used. Use it to compare last year’s taxable income to your current year estimate.

- Filing status: single, married filing jointly, married filing separately, head of household, or qualifying widow(er). Your filing status changes bracket cutoffs and standard deduction amounts.

- Estimate of other income: interest, dividends, capital gains, retirement distributions, rental income, and self-employment earnings. Those flow into adjusted gross income (AGI) and can push you into a higher bracket.

- Planned deductions: decide whether you’ll use the standard deduction or itemize (mortgage interest, state and local taxes capped, charitable gifts, medical expenses above the AGI threshold). The standard deduction is automatically inflation adjusted each year — check the IRS website for the exact 2026 dollar amounts when available.

- Access to IRS tools and instructions online: the IRS news releases on inflation adjustments and the Form W-4 page. Useful URLs: https://www.irs.gov/newsroom and https://www.irs.gov/forms-pubs/about-form-w-4. Also use the IRS Tax Withholding Estimator at https://www.irs.gov/individuals/tax-withholding-estimator.

Step-by-step: find your 2026 tax bracket and estimate tax

Walk through these steps to find your 2026 bracket and estimate your federal tax bill.

- Confirm your filing status. That determines which table to use. Married filing jointly uses the higher joint thresholds above. Married filing separately is typically half of the joint cutoffs; head of household uses its own table.

- Calculate gross income. Add wages, self-employment income, interest, dividends, retirement distributions, and other taxable receipts. That gives your total gross income for the year.

- Compute adjusted gross income (AGI). Subtract adjustments allowed above-the-line — retirement plan contributions, student loan interest (if eligible), self-employment deductions, health savings account contributions, and certain moving or educator expenses if applicable. AGI is the basis for many credits and deductions.

- Choose standard deduction vs. Itemize. Subtract the standard deduction or your total itemized deductions to get taxable income. The standard deduction is indexed annually; check the IRS site for the 2026 exact figures. If your itemized deductions (mortgage interest, state and local tax up to the SALT cap, charitable donations) exceed the standard deduction, itemize.

- Locate the bracket thresholds. Use the quick-reference table above for the marginal rate thresholds. Taxable income falls into a marginal rate based on the highest bracket touched. But your entire income isn’t taxed at that top rate — only the portion above the bracket threshold is.

- Compute tax by bracket. Tax each slice of your taxable income at its bracket rate, then add those amounts together — that gives you your preliminary tax liability. For example, a single filer with $200,000 taxable income in 2026 would pay: 10% on the first $12,400, 12% on the next slice up to $50,400, 22% up to $105,700, 24% up to $201,775 — and the remaining amount in the 24% bracket. Use a spreadsheet or the IRS tax tables to speed this step.

- Factor in tax credits. Subtract nonrefundable credits first (child tax credit if applicable, education credits, saver’s credit). Then apply refundable credits (additional child tax credit, earned income tax credit). Credits reduce tax dollar-for-dollar and can change whether you owe or get a refund.

- Compare withholding and estimated tax payments. Add federal tax withheld from paychecks and any estimated tax payments you made. If total payments are less than your computed tax, you’ll owe the balance and might face underpayment penalties. If payments are more, you’ll get a refund.

- Adjust withholding if needed. If you expect a large balance due or a very large refund, update your Form W-4 with your employer or increase/decrease estimated quarterly payments. Use the IRS Tax Withholding Estimator to calculate the exact withholding changes: https://www.irs.gov/individuals/tax-withholding-estimator.

Example calculation (simple)

Quick example to show the marginal rates in action. Use the 2026 thresholds above.

Single filer. Taxable income: $200,000.

- 10% on first $12,400 = $1,240.

- 12% on $12,400–$50,400 ($38,000) = $4,560.

- 22% on $50,400–$105,700 ($55,300) = $12,166.

- 24% on $105,700–$200,000 ($94,300) = $22,632.

Total federal income tax before credits = $40,598. Credits and other taxes (AMT, self-employment tax) would modify the final amount.

Tips for 2026

- But don’t assume rates change — they didn’t. The 10%–37% marginal rates stayed the same for 2026, so inflation adjustments are what matter.

- Plan for bracket creep relief. With thresholds up, a raise is less likely to push you into a higher bracket immediately — yet increases to income that raise AGI can still reduce phaseouts and affect credits.

- Consider timing income and deductions. If you can accelerate deductions into 2026 or defer income to 2027, do the math to see if that lowers your tax bill. This is especially important for people near top ends of brackets.

- Use the IRS withholding tools. Update Form W-4 if your life changed — marriage, new job, new child — or if your withholding kept producing big refunds or balances.

- Self-employed? Make estimated quarterly payments using Form 1040-ES to avoid penalties. The due dates are usually April, June, September and January of the following year.

Common mistakes to avoid

- Failing to use taxable income. Don’t compare your gross pay to bracket cutoffs. Always subtract adjustments and deductions first.

- Ignoring other taxes. Social Security and Medicare withholding, self-employment tax, and the Net Investment Income Tax can affect your total tax bill even though they’re not part of the bracket table.

- Relying on year-old withholding. A job change, side hustle, or retirement distribution changes withholding needs. Recalculate mid-year if anything big happens.

- Overlooking credits. Child tax credit, earned income tax credit, education credits, and energy credits can drive your tax liability down or create refunds — check eligibility.

- Missing deadlines. File on time or file an extension and pay any estimated balance by the original due date to limit penalties and interest.

For authoritative details, IRS pages to bookmark include the 2026 inflation adjustments news release at https://www.irs.gov/newsroom and the Form W-4 instructions at https://www.irs.gov/forms-pubs/about-form-w-4.

Related Articles

- NJ property tax appeal 2026: filing steps

- FAFSA cost of attendance 2026

- How to apply smart broadband plan in 2026

Brackets for 2026 keep the familiar 10%–37% rates, but thresholds rose for inflation — that softens bracket creep. Use the quick-reference thresholds above, run the step-by-step estimate, then adjust withholding or estimated payments if you expect a big balance or refund. Check the IRS site and the Tax Withholding Estimator before making major moves.