For married couples filing jointly, the 2026 tax year features higher income thresholds for each federal tax bracket. This means more of your income is taxed at lower rates, and less is taxed at the highest rates. This guide lays out the 2026 tax brackets for married filing jointly, explains how to calculate your tax step-by-step, lists necessary documents and IRS forms, and offers tips on adjusting withholding, estimating payments, and planning for 2026 taxes.

Quick-reference: 2026 brackets (Married Filing Jointly)

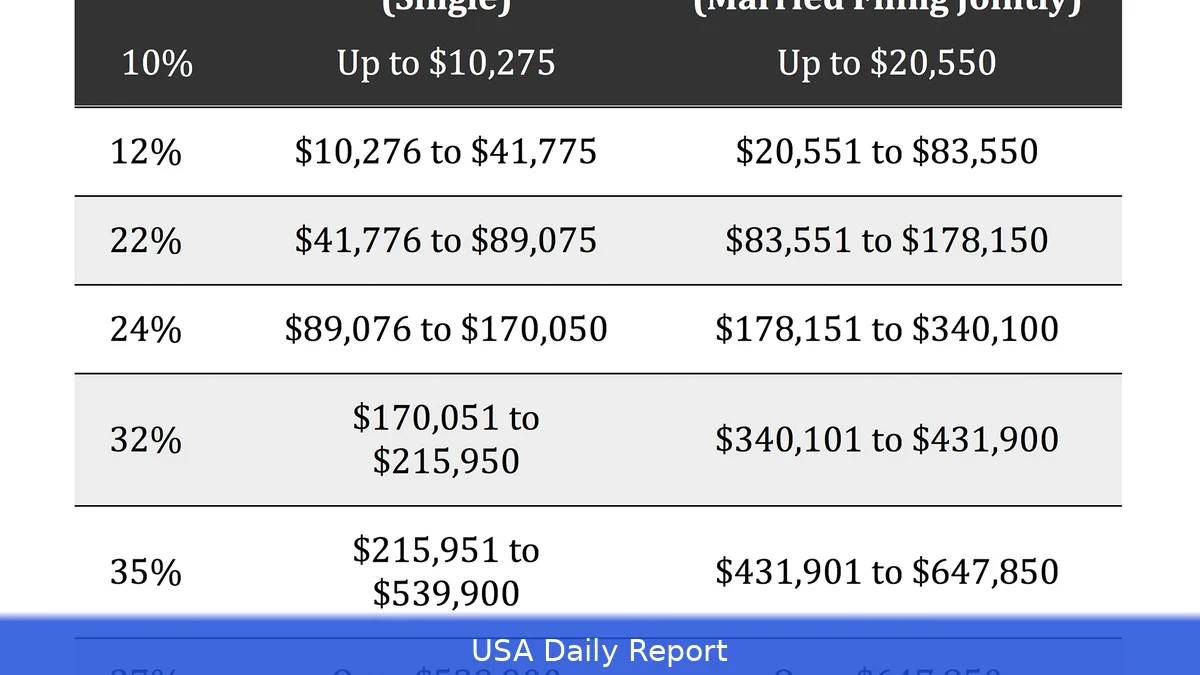

Refer to this table to find the marginal tax rates for your taxable income in 2026, with returns filed in 2027. These brackets reflect the federal income tax rates for married couples filing jointly, adjusted for inflation in 2026.

| Tax Rate | Taxable income (2026, MFJ) |

|---|---|

| 10% | $0 to $24,800 |

| 12% | Over $24,800 to $100,800 |

| 22% | Over $100,800 to $211,400 |

| 24% | Over $211,400 to $403,550 |

| 32% | Over $403,550 to $512,450 |

| 35% | Over $512,450 to $768,700 |

| 37% | Over $768,700 |

Standard deduction (2026): $32,200 for married couples filing jointly; $16,100 for single filers. Returns for tax year 2026 are due mid-April 2027 (typically April 15, 2027) unless the date moves for a weekend or holiday; if you file an extension, the extended deadline is typically mid-October 2027.

Prerequisites — what to have before you calculate

Gather these documents and accounts first to save time and prevent mistakes.

- Income documents: W-2s from employers, 1099-NEC for contractor pay, 1099-MISC for other payments, 1099-INT for interest, 1099-DIV for dividends, 1099-R for retirement distributions.

- Records of adjustments: IRA contribution receipts, HSA contribution statements, Form 5498, student loan interest paid, educator expenses and self-employed health insurance receipts.

- Deductions and credits backup: mortgage interest (Form 1098), state and local tax records, charitable receipts, child care provider info and EIN for claiming the Child and Dependent Care Credit.

- Account access: login for IRS.gov, access to your employer payroll portal to change withholding, and your tax-software or CPA contact info.

- IRS resources and forms you may need: Form 1040 (https://www.irs.gov/forms-pubs/about-form-1040), Schedule A for itemized deductions (https://www.irs.gov/forms-pubs/about-schedule-a-form-1040), Form W-4 to change withholding (https://www.irs.gov/forms-pubs/about-form-w-4), and the IRS Tax Withholding Estimator (https://www.irs.gov/individuals/tax-withholding-estimator).

How the brackets work — quick primer

Marginal tax brackets divide your taxable income into portions. You don’t pay a single rate on all your income; instead, each portion is taxed at its bracket’s rate. That means entering a higher bracket only taxes the income above that threshold at the higher rate.

Example: the first $24,800 of taxable income for MFJ is taxed at 10%. Income between $24,800 and $100,800 is taxed at 12%, and so on. Your taxable income equals adjusted gross income (AGI) minus either the standard deduction ($32,200 for MFJ in 2026) or itemized deductions.

Step-by-step: Calculate your 2026 federal income tax (MFJ)

Use these steps to estimate your federal income tax for 2026. While tax software or spreadsheets improve accuracy, these manual steps help you grasp the calculations.

- Gather documents. Have all W-2s, 1099s, and receipts ready. If you expect business income, get profit/loss statements and Schedule K-1s. For rental or investment income, pull 1099s and brokerage statements.

- Compute gross income and adjustments. Add wages, interest, dividends, business income, capital gains, rental income and other receipts to get gross income. Subtract adjustments like traditional IRA contributions, HSA deposits, student loan interest (up to the applicable limit), and self-employed retirement contributions to get adjusted gross income (AGI).

- Choose deductions. Compare the standard deduction ($32,200 MFJ) to itemized deductions on Schedule A. Itemize if the total of mortgage interest, state and local taxes (SALT — limited to $10,000 combined for 2018-2025 rules unless changes apply), charitable gifts, and medical expenses above the AGI floor exceeds the standard deduction.

- Calculate taxable income. Taxable income = AGI minus deduction (standard or itemized) and any qualified business income deduction (if eligible). Round down to the nearest dollar.

- Apply the 2026 bracket math. Break your taxable income into the bracket slices shown above, multiply each slice by its rate, and add the results. That gives your preliminary tax before credits. For clarity, here's how to compute tax for a taxable income of $300,000:

Worked example: married filing jointly, $300,000 taxable income

Compute tax by bracket:

- 10% on first $24,800 = $2,480

- 12% on $76,000 (that is $100,800 − $24,800) = $9,120

- 22% on $110,600 (that is $211,400 − $100,800) = $24,332

- 24% on $88,600 (that is $300,000 − $211,400) = $21,264

Here's the thing — add them: $2,480 + $9,120 + $24,332 + $21,264 = $57,196 federal tax before credits. Then subtract any tax credits (child tax credit, energy credits, education credits). For example, a $2,000 Child Tax Credit per qualifying child under age 17 reduces tax dollar-for-dollar.

Adjust withholding and estimated payments — exact steps

Take action now to avoid surprises at tax time.

- Use the IRS Tax Withholding Estimator. Go to https://www.irs.gov/individuals/tax-withholding-estimator, enter your filing status (Married Filing Jointly), projected 2026 income, deductions, and credits. The tool gives recommended federal income tax withholding per paycheck.

- Update Form W-4 with your employer. To change withholding, fill out a new Form W-4 (https://www.irs.gov/forms-pubs/about-form-w-4). Complete Steps 1 and 5; use Step 3 for claiming dependents (e.g., $2,000 per qualifying child), Step 4 for other adjustments (other income, deductions other than the standard deduction, extra withholding). Sign, date, and submit it to payroll.

- Make estimated tax payments if needed. If you expect tax not covered by withholding — from freelance work or investment income — make quarterly estimated payments using Form 1040-ES vouchers or via IRS Direct Pay at https://www.irs.gov/payments. Estimated payments for 2026 are typically due in April, June, September 2026 and January 2027; check Publication 505 for exact dates.

Tips for lowering taxable income in 2026

- Contribute pre-tax to employer retirement plans. Check your plan limit with your HR department — traditional 401(k) deferrals reduce taxable wages immediately.

- Max HSA contributions if you have a high-deductible health plan — HSA deposits are tax-deductible and grow tax-free. For family coverage, confirm the 2026 HSA limits on IRS.gov.

- Time deductible expenses. If you’re near the itemizing threshold, bunch charitable gifts or medical expenses into one year to exceed the standard deduction and itemize that year.

- Claim eligible tax credits. Child Tax Credit remains $2,000 per qualifying child under 17 for the post‑2021 rules; check eligibility rules on IRS pages and Form 1040 instructions.

Common mistakes to avoid

- Not updating your W-4 after a major life change (marriage, new job, second job, or new child). That can lead to under-withholding and penalties.

- Overlooking non-wage income. Self-employment, rental income, and large investment gains need quarterly estimated tax payments or higher withholding.

- Double counting deductions. If you take the standard deduction, don’t list the same items on Schedule A. Keep receipts but don’t claim both.

- Ignoring the alternative minimum tax (AMT). For couples with large tax preference items or big deductions, run an AMT check — tax software flags it, or see IRS Form 6251 instructions.

- Waiting until April. Adjust now if 2026 withholding looks off. Mid-year adjustments smooth cash flow and avoid big tax bills in 2027.

Related Articles

- Best tax brackets 2026: which brackets to target and why

- How to file taxes as a 1099 contractor in 2026

- How to apply for federal income tax (2026): step-by-step guide

Use the 2026 married filing jointly brackets to plan withholding, retirement contributions, and estimated payments. Run the numbers now with the IRS Tax Withholding Estimator, update your Form W-4 through your employer, and file Form 1040 next April 2027 with Schedule A if you itemize. Check IRS.gov for forms, Pub. 505 for withholding and estimated tax guidance, and update plans if income or family status changes.