Tax year 2026 is full of tough decisions. Changes in rates, thresholds, and reporting rules can really affect how much tax you pay and what stays in your pocket. Here’s a guide that ranks the most useful U.S. federal tax brackets for 2026, shows how to target them, points out common pitfalls, and breaks down the key dollar impacts.

Quick reference — best tax brackets 2026 at a glance

- Best bracket to target for Roth conversions: 12% (low-to-moderate taxable income).

- Best bracket for maximizing retirement savings while keeping marginal tax low: 22% (mid earners who can still save pre-tax).

- Best bracket for low earned-income tax credit and benefits: 10% to 12% zone.

- Best bracket for charitable bunching: 24% (larger deduction value).

- Watch-outs: hitting 32% or 35% sharply increases marginal taxes and Medicare IRMAA exposure for high earners.

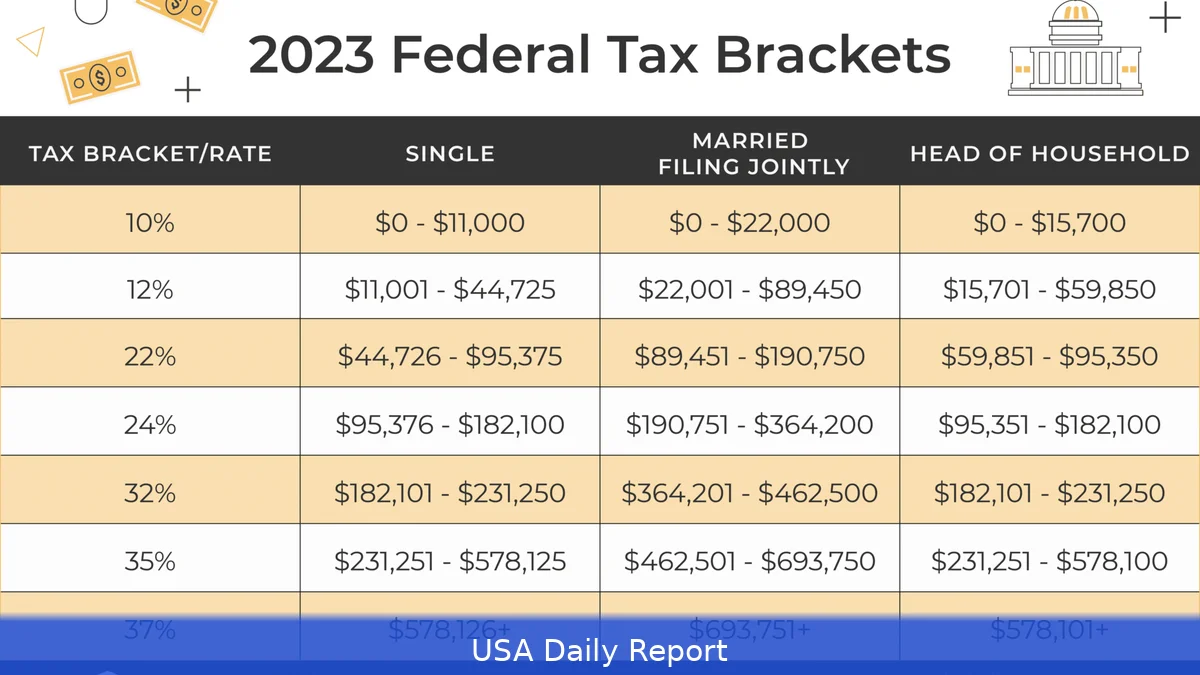

Quick facts you’ll want now: the federal marginal-rate set still used across most planning is the seven-rate schedule (10%, 12%, 22%, 24%, 32%, 35%, 37%). For retirement savings, the 2026 401(k) employee elective deferral limit is $24,500, and catch-up contributions for employees aged 50+ are $8,000. The 1099-K threshold reverted in federal law in 2025 to $20,000 and 200 transactions, though several states maintain a $600 state-level reporting threshold that affects gig sellers and side-hustles.

How this ranking works

We looked at tax brackets and bands based on how useful they are for different households in 2026 — which ones help with tax-saving moves like Roth conversions and credits, which balance tax rates and flexibility, and which ones come with risks. Each item below lists key features, pros, cons, who it's best for, and an illustrative pricing example in USD — what federal tax looks like at a representative taxable income inside that band.

Ranked list — Best tax brackets (1–10)

1. 12% marginal rate — Best overall place to land for conversions and credits

Key features: Low single-digit marginal tax. Ideal window for partial Roth conversions, harvesting long-term capital gains at low tax impact, and for families qualifying for many refundable credits. It’s often the best spot for workers who have a temporary income dip, like during a job change or sabbatical.

Pros: This bracket makes it cheaper to start Roth IRA conversions. Keeps phase-ins for tax credits and reduced Medicare IRMAA exposure easier to manage. Low marginal hit on retirement withdrawals.

Cons: Narrow band — move a bit higher and the next dollars face 22% or higher. Not useful if household income is chronically above the band.

Who it’s best for: Mid-career savers doing strategic Roth conversions, families claiming refundable credits, lower-middle-income earners who want to avoid higher brackets.

Pricing example (illustrative): Tax on an additional $10,000 of taxable income inside the 12% bracket = $1,200 federal tax.

2. 22% marginal rate — Best mix of earning and saving

Key features: The workhorse bracket for many middle-class taxpayers. Holds room for pre-tax retirement savings (401(k), traditional IRA) while still keeping marginal tax reasonable.

Pros: Good compromise: you earn more but don’t jump to top-tier rates. Tax-deductible retirement deferrals and HSA contributions still buy meaningful tax reduction.

Cons: Higher marginal rate means Roth conversions cost more. Phaseouts for some credits begin to bite here.

Who it’s best for: Households earning steady wages in the middle-income range who can stash significant amounts into retirement accounts but want to avoid top brackets.

Pricing example (illustrative): Tax on an extra $10,000 inside 22% = $2,200 federal tax.

3. 24% marginal rate — Best for charitable deduction strategies

Key features: Once households hit this band they often benefit from itemizing — especially if they bunch charitable gifts into alternate years or use donor-advised funds.

Pros: Greater marginal value from deductions — a $10,000 deductible gift reduces federal tax roughly by $2,400 at the margin. Good target for charitable bunching and for using Qualified Charitable Distributions (QCDs) from IRAs if age-qualified.

Frankly, cons: Still significantly higher than the low brackets. Social Security and Medicare surtax exposure for higher-income households begins to matter when combined with other income.

Who it’s best for: Wealthier retirees and high-saving households who want to optimize charitable giving and itemized deductions.

Pricing example (illustrative): $10,000 gift at 24% saves about $2,400 in federal tax.

4. 10% marginal rate — Best for low-income households and maximizing refundable credits

Key features: The bottom rung. Many low-income workers and early-career taxpayers fall here after the standard deduction. Keeps payroll withholding light and maximizes take-home pay.

Pros: Low marginal taxes; easier qualification for Earned Income Tax Credit (EITC) and certain refundable credits. Minor Roth conversions are cheap here.

Cons: Limited room for tax sheltering. Low tax liability means pre-tax retirement deferrals provide smaller current-year tax shields in absolute dollars.

Who it’s best for: Entry-level workers, part-time earners, students with earnings, families relying on refundable credits.

Pricing example (illustrative): $10,000 additional taxable income in the 10% bracket = $1,000 federal tax.

5. 32% marginal rate — Best for targeted timing of income and deductions

Key features: A clear warning sign: at 32% you lose a lot of tax base per extra dollar. But it’s also a place where careful timing of income and deductions (capital gains, business profits, retirement distributions) can yield big savings.

Pros: If income is lumpy, shifting gains or deductions to a year you’re below this band can save big dollars. Tax-loss harvesting helps here.

Cons: High marginal cost; increased chance of AMT or net investment income surtax exposure. Medicare IRMAA premiums can jump for single-year spikes.

Who it’s best for: High earners with flexible timing for income or deductions, and business owners who can time income recognition.

Pricing example (illustrative): $10,000 additional taxable income at 32% = $3,200 federal tax.

6. 35% marginal rate — Best for strategic long-term planning

Key features: Deep into high-income territory. Households here need long-range moves: Roth conversions over multiple years, tax-efficient investments, charitable strategies, family gifting and estate planning.

Pros: Many tax-minimization tactics pay off because each dollar saved avoids a large tax hit.

Cons: Less room to move in a single year. Exposure to additional levies — Net Investment Income Tax (3.8%), potential state taxes and Medicare surcharges.

Who it’s best for: Top earners with access to tax planning tools, business owners, and families looking to shift wealth.

Pricing example (illustrative): $10,000 extra taxable income at 35% = $3,500 federal tax.

7. 37% marginal rate — Worst marginal rate but unavoidable for highest earners

Key features: Top marginal U.S. Federal bracket for ordinary income. High cost of mistakes and of failing to plan around large one-time income events.

Pros: Not many; mostly a signal to aggressively seek tax efficiency.

Cons: High tax on extra income, plus likely exposure to surtaxes and higher state taxes. Retirement withdrawals and conversions here are expensive.

Who it’s best for: It’s not a bracket you 'choose' — it's where very high earners end up. The goal is usually to manage taxable income so fewer dollars sit in this zone.

Pricing example (illustrative): $10,000 extra taxable income at 37% = $3,700 federal tax.

8. 0% long-term capital gains bracket — Best tax-free gains window

Key features: If taxable income (including gains) stays low enough, long-term capital gains and qualified dividends can be taxed at 0% federally.

Pros: Huge win for retirees or anyone with low ordinary income who can sell appreciated investments without federal tax.

Cons: The 0% window is income-sensitive — adding ordinary income can push gains into 15% or 20% capital gains rates.

Who it’s best for: Retirees, lower-income investors, phased retirement workers.

Pricing example (illustrative): Selling $50,000 of long-term gain while taxable income stays in the 0% gains window = $0 federal tax on the gain.

9. Alternative Minimum Tax (AMT) band — Best for watching triggers

Key features: AMT isn’t a single marginal rate like ordinary tax brackets. It’s a parallel calculation that can bite taxpayers with many deductions or certain types of income.

Pros: Once AMT is triggered, planning options change — knowing thresholds helps prevent surprises.

Cons: Complex. AMT has its own exemptions and phaseouts and can eliminate the benefit of many itemized deductions.

Who it’s best for: High earners with large state taxes, multiple dependents, or accelerated incentive stock option exercises.

Pricing example (illustrative): AMT liability can add thousands in tax; for example, a conversion that costs $10,000 ordinary tax under regular rules might trigger AMT effects that add several thousand more in tax.

10. Net Investment Income Tax (NIIT) band — Best to avoid if possible

Key features: A 3.8% surtax that applies to investment income above certain modified adjusted gross income thresholds.

Pros: None — it’s an extra tax. But it’s predictable, so planning can reduce exposure.

Cons: Applies in addition to federal marginal tax on investment income. Hard to escape if MAGI is high.

Who it’s best for: The goal is to avoid it. Best for people who can time sales, use tax-advantaged accounts, or shift income across years.

Pricing example (illustrative): If $20,000 of investment income is subject to NIIT, that’s $760 in additional federal tax (3.8%).

How to aim for the right bracket in 2026 — step-by-step

1) Project taxable income. Start with wage income, expected retirement distributions, expected capital gains and business profit for 2026. Include side-hustle receipts — remember several states still require 1099-K reporting at $600 even though federal law set a $20,000/200-transaction threshold.

2) Add expected adjustments: pre-tax 401(k) deferrals, HSA deposits, traditional IRA deductible amounts. For 2026, elective deferrals are $24,500 and catch-up is $8,000 for those 50+.

3) Model scenarios: do a no-change run, a Roth conversion run, and a high-contribution run. See which years push you into higher brackets or surtaxes.

4) Time income and deductions: shift gains to years you’re in the 12% or 0% gains window, bunch deductions like charitable gifts or medical expenses, and delay nonessential retirement withdrawals.

5) Re-check payroll withholding and estimated tax payments quarterly — many surprises in 2026 stem from under-withholding and 1099 mismatches.

Common mistakes to avoid

- Ignoring state rules on payment reporting: several states kept a $600 1099-K reporting requirement after federal law changed. That can create surprising state tax notices.

- Letting Roth conversions pile into a single year — spread conversions across several years to avoid hitting 24%/32% thresholds.

- Forgetting catch-up rules. For 2026, if eligible, the $8,000 catch-up adds big tax-free retirement capacity.

- Not planning around RMDs and Medicare IRMAA. Required minimum distributions now start at age 73; they can push retirees into higher brackets and increase Medicare Part B/D premiums.

- Treating taxable income as stable when it's lumpy. One-time business sales, option exercises or bonus years need special handling.

Alternatives and comparisons

- Roth conversions vs. Tax-deferred saving: Roth conversions pay tax now but shield later withdrawals. If the marginal rate today is 12% and you expect 22% in retirement, convert now. If you expect much lower rates later, lean traditional.

- Harvesting capital losses vs. Deferring gains: Selling losers to offset gains is cheap tax insurance. In years where ordinary income is low enough to fall into the 0% gains window, realize gains instead of losses.

Costs, fees and eligibility to watch

- Tax prep and planning fees: Simple returns may cost $0–$150 with DIY software; complex returns involving AMT, business schedules or large Roth conversions can cost $500–$3,000 with professional help. Good CPAs and enrolled agents typically charge by complexity, not bracket.

- Penalties: Underpayment penalties apply if estimated taxes are too low; filing late can trigger penalties and interest. Avoid surprises by adjusting withholding or making quarterly estimated payments when converting or selling assets.

- Eligibility: Certain credits and deductions phase out by AGI or MAGI — know the phaseout ranges for child tax credits, Earned Income Tax Credit, education credits and more.

How we chose and what to watch in 2026

This ranking prioritizes practical value — the real tax dollars saved or cost avoided by landing inside a bracket. We weighed conversion opportunities, deduction leverage, exposure to surtaxes (NIIT, IRMAA), and common real-world situations (side gigs, retirement, capital gains). Watch for changing law: 2026 still carries carryover politics from the end of the TCJA era and state-level reporting changes. Those shifts affect where it pays to be on the income scale.

Related Articles

- How to file taxes as a 1099 contractor in 2026

- How much is self-employment tax in 2026: rates, caps, examples, and how to calculate it

- How to apply for federal income tax (2026): step-by-step guide

Target the lower middle brackets when possible — that’s where conversions, tax-free gains and credit access buy the most. Use deferrals, Roth conversions spread across years, charitable bunching and timing of gains to keep peak taxable income out of the 32%+ zone. And remember: tax brackets aren’t just numbers — they’re a planning map. Adjust withholding, watch your state rules (1099-K can still kick in at $600 in some states), and get a quarterly check-in with your tax pro if your income’s lumpy. Tax day 2026 is April 15, 2026 — plan before then if you want to change what bracket you’ll occupy.