Mortgage rates have dropped below 6%, which is good news for buyers and homeowners. But experts say don’t expect a rapid drop anytime soon — 2026 may be a year of steady or slowly declining rates instead.

Rates Edge Below 6%, But The Market Remains Cautious

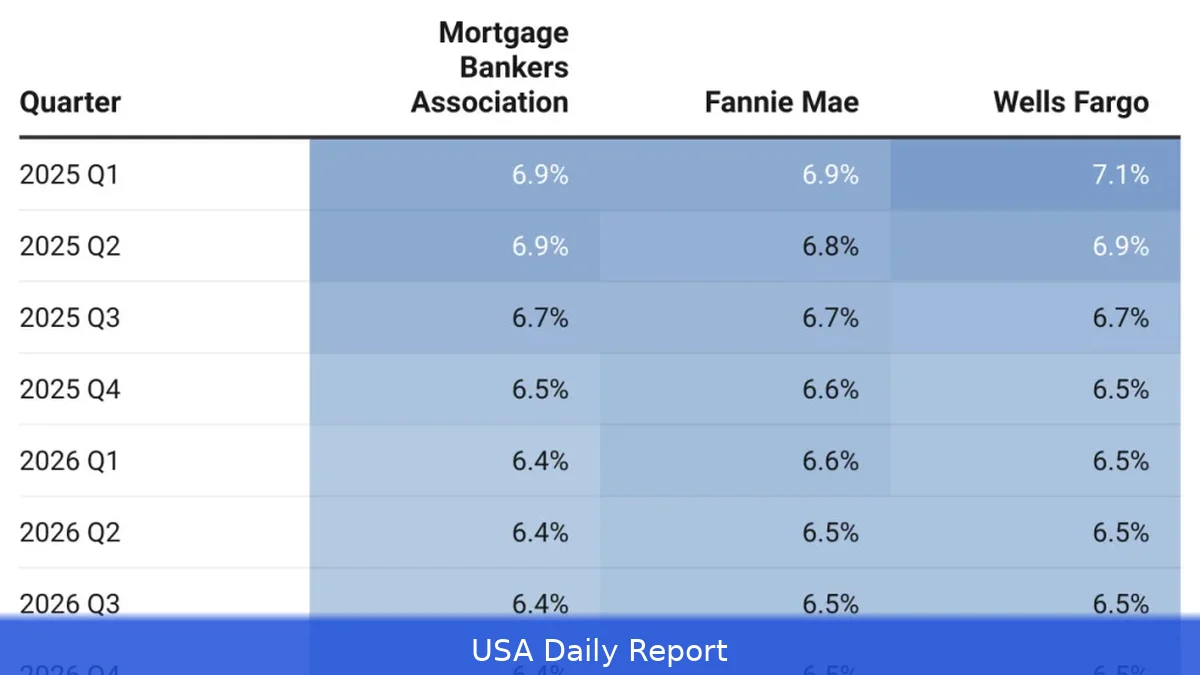

By early March 2026, the average 30-year fixed mortgage rate had slipped to just under 6%, according to Zillow data. The 30-year rate hovered around 5.87% on March 3 and crept up slightly to 5.99% by March 9. Meanwhile, 15-year fixed rates were sitting around 5.37% to 5.50%, offering some affordable options for borrowers seeking shorter loan terms.

This is a big change from late 2023 when 30-year rates hit as high as 7.79%, putting homeownership out of reach for many. The drop has come after six Federal Reserve rate cuts totaling 1.75%, along with easing inflation and falling Treasury yields.

But the market is still cautious. Rates have improved only gradually over the past two years. Andrew Postell, VP of mortgage lending at Rate.com, said the weekly changes might seem small, but over time they add up to big savings. "We are nearly two points lower on the average interest rate from October 2023."

Fed Holds Steady, Adding to Rate Stability

Since late 2025, the Federal Reserve hasn't changed its target interest rates and is expected to keep them steady through March 2026. The Fed’s March 17-18 meeting will be closely watched, though experts predict no change.

Mark Schweitzer, associate professor of economics at Case Western Reserve University, said mortgage rates will likely stay steady in March unless fresh economic data changes the outlook. He pointed to the upcoming Consumer Price Index report on March 11 as a key signpost.

"Market expectations favor no change in the Fed funds rate," Schweitzer noted. The Fed’s cautious approach reflects ongoing uncertainty in inflation trends and employment data, which both influence bond yields and mortgage rates.

Refinancing Opportunities For Homeowners

People who got mortgages at high rates in 2023 and 2024 might want to consider refinancing now. The average refinance rate on a 30-year loan dropped to 6.34% by March 9, down from roughly 6.50% earlier in the year. For 15-year refinances, the median rate was near 5.39% in early March.

Refinancing can help homeowners cut monthly payments or shorten their loan terms, but experts advise caution.

"Don’t rush into refinancing," said industry insiders. It’s most worthwhile for those planning to stay in their homes long enough to recoup closing costs and fees. Shopping around for competitive rates and terms remains critical.

What Could Drive Rates Next?

A few things could push mortgage rates up or down as 2026 goes on.

First, Treasury yields — especially the 10-year note — play a major role. A gradual decline in yields has helped push rates down recently, but any jump in yields could reverse that trend.

Second, inflation data remains a wildcard. The Consumer Price Index dipped from 2.7% in December 2025 to 2.4% in January 2026, easing pressure on rates. If inflation slows further, rates could fall. But if inflation picks up again, the Fed may reconsider its policy stance.

Finally, unemployment figures and broader economic signals will shape investor confidence and demand for mortgage-backed securities, influencing borrowing costs.

Mortgage rates look better for buyers and refinancers compared to last year, but a big drop isn’t likely. Steady or slightly falling rates seem the best bet for 2026, with key economic data points holding the market’s attention.