Investors pushed Chinese rare-earth shares higher this week. The move followed Beijing’s tighter export posture and fresh signs of market repricing. Traders are betting supply will be tighter and prices firmer this quarter.

Why shares moved

The market moved quickly. Shares of companies tied to rare-earth mining and processing rallied after reports that China has been tightening controls on the flow of critical minerals, prompting traders to mark up the likely near-term price for key elements like neodymium and dysprosium.

The move went beyond headlines. China controls a large share of the rare-earth chain—from reserves through magnets—so even small signs of constrained supply make buyers act now.

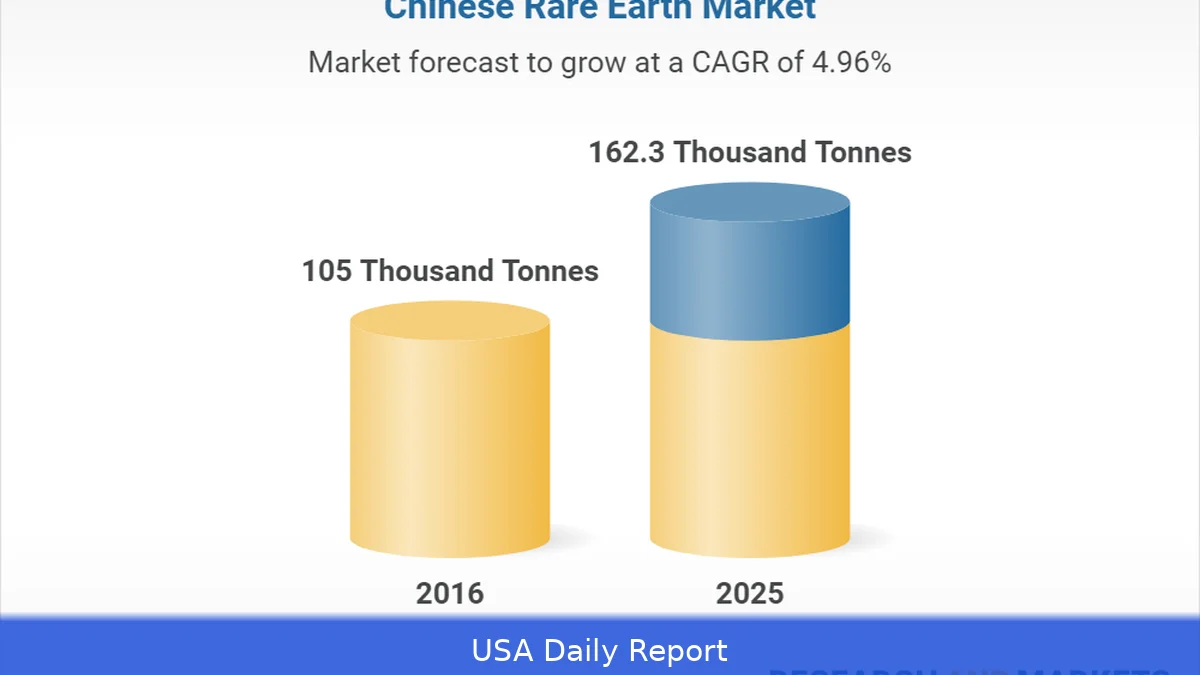

Beijing's edge comes down to production and processing scale, not necessarily a technology lead. China accounts for roughly half of identified global reserves, around two-thirds of mining, and an even larger share of refining and magnet manufacturing.

Those figures matter when global buyers and chipmakers race for inputs that go into electric-vehicle motors, wind turbines and advanced electronics.

Because production and processing are concentrated, even short-term export changes can alter prices. Manufacturers facing tighter access bid more for inputs, and that prospect can lift producers' valuations.

Supply chain and environmental baggage

This isn't only a geopolitical story. China's rare-earth industry has long relied on lower labor costs and laxer environmental enforcement — factors that helped it scale refining and separation faster than rivals. But that came with costs.

Pollution linked to rare-earth refining has left environmental and public-health scars in regions such as Baotou and Ganzhou. Localized contamination episodes and health concerns showed up in the past decade, and they've helped shape how quickly other countries moved to develop rival capacity.

Still, building the type of refining and magnet-making capacity that China has isn't quick or cheap. So even companies outside China that win new mines face a multi-year bottleneck at the refining stage. That delay feeds into price expectations today — and into share moves.

Global market reaction

Markets focus on near-term risks, not distant plans—traders price what could tighten in the next quarter. When President Donald Trump publicly threatened higher tariffs on Chinese imports and suggested canceling a summit with Chinese leader Xi Jinping after reports of Beijing curbing rare-earth exports, U.S. Equities felt the ripple.

U.S. Tech stocks were especially sensitive. Semiconductor names and AI-related firms fell as investors priced in higher input costs and a tougher trade backdrop. At the same time, firms whose margins are less exposed to supply shocks — consumer staples, for example — held up better.

That selloff in U.S. Tech helped amplify the relative appeal of producers closer to the resource source. Investors rotated money toward firms that stand to benefit, at least soon, from firmer rare-earth prices or tighter availability.

How this ties to inflation and Fed policy

The move came as inflation readings cooled and markets anticipated Fed easing—factors that can change risk appetite. A lighter CPI print had already nudged markets toward the view that policy would ease — and that made resource-driven rallies more plausible because lower rates tend to support risk assets.

Federal Reserve Chair Jerome Powell has kept officials focused on jobs and price signs, while markets try to reconcile potential easing with fresh supply-side risks from geopolitics. That balancing act matters because it shapes how investors value future earnings when input costs jump.

Who wins and who loses

Raw-material producers and refiners see the clearest short-term gain if prices rise. Companies selling magnets or separated rare-earth oxides can report stronger margins in a quarter where their realized prices climb — provided they can maintain output.

Buyers deeper in the chain — chipmakers and EV manufacturers — will feel pressure on margins if costs rise and they can't pass those increases onto customers. For them, higher rare-earth quotes mean either absorbing costs or raising prices on electronics and vehicles.

Governments are part of the tradeoff too. Some countries have accelerated plans to build local refining and recycling capacity precisely because of episodes like this. But scaling those projects takes years and capital; the market's current repricing is happening now.

Longer-term context

Analysts who study the sector say Beijing's leverage is strongest in the short run because of the structure of the value chain. Over time, environmental cleanup, higher labor costs and foreign investment in processing could erode that edge. Still, the lead time is long.

For investors that usually means volatility: export-related price spikes can quickly lift producers and squeeze downstream buyers, until new mines, recycling or processing capacity eventually shifts the balance.

What traders are watching next

Market participants will be watching a few things closely: any firm announcements of export quotas or price guidance from major Chinese producers; official statements from Beijing on export policy; and updates from potential alternative suppliers in Australia, the U.S. And elsewhere.

On the macro side, traders will track the Fed's moves and economic data that influence risk appetite. If interest-rate expectations shift toward more easing, that could amplify rallies in resource stocks. If policy stays tighter, higher financing costs could mute some of those gains.

And of course, bilateral talks between the U.S. And China can calm nerves — or inflame them. A meeting between President Trump and Xi Jinping on the sidelines of global summits will be parsed for any trade or export signals.

Related Articles

- Asian LNG Spot Prices Surge After Strait of Hormuz Closure, Supply Shortfall Looms

- Global Bonds Slide After US‑Iran Talks Fail, Investors Fear Inflation Will Stick

- Vitol Shuffles London Derivatives Desk After Mark-to-Market Losses

"Despite the lack of labor market data due to the government shutdown, this lighter-than-expected CPI report should offer a confidence boost to a Federal Reserve that already appeared inclined toward additional rate cuts in October and December," said Stephen Kates, Bankrate analyst.