Energy and shipping risks are rattling markets. If Spain urged China to step in, traders would notice.

Frontline facts traders care about

Conflict in Ukraine is still producing humanitarian needs on the ground. Volunteers and aid workers are sending simple items—handmade candle stoves among them—to give people heat and light where power's gone out, according to reporting by BBC News. Those are small signals of the bigger problem: fighting damages infrastructure, and damaged infrastructure has costs that ripple through economies.

So what looks like charity at the front lines turns into balance-sheet issues farther back.

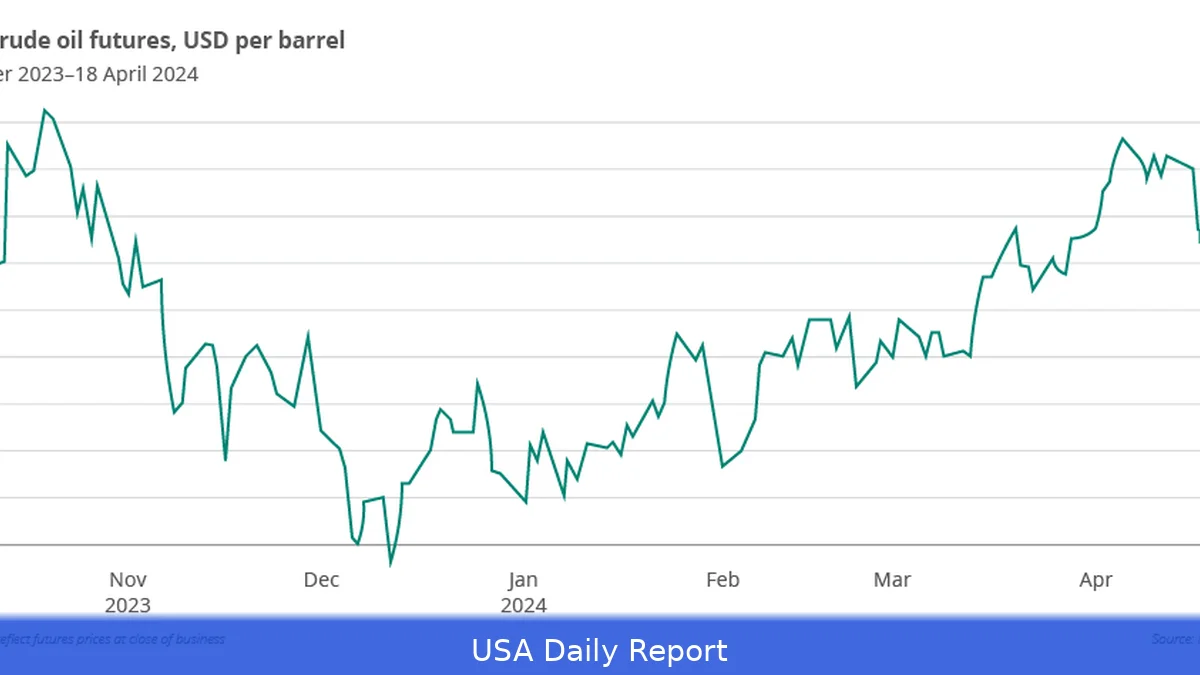

Meanwhile, tensions around Iran are ratcheting up at a strategic choke point for energy and trade. U.S. Central Command has signaled a possible blockade of Iranian ports beginning Monday, while saying ships can still transit the Strait of Hormuz to and from non‑Iranian ports, according to Al Jazeera's coverage. That's a precise operational detail — and an important one for shipping flows and insurance costs.

Humanitarian needs in Ukraine and the U.S. threat of a blockade on Iranian ports are the immediate issues investors will watch; they'll change how some traders size positions and buy protection. The immediate channels are obvious: oil flows, shipping routes, and insurance premia. But the ways those channels feed into markets are messy and fast-moving.

How risk translates to prices

Traders ignore grand narratives; they act on likely supply, demand and transport costs, so when supply looks shaky they start hedging now. When a major exporter faces the prospect of port closures or when infrastructure is knocked out by war, buyers start hedging. They raise bids. They push up futures. That's basic.

Expect quick price jumps and follow-on costs — freight bills and insurance often jump first, and those added expenses get passed down the chain. That re-pricing then shows up in consumer-facing numbers: fuel at the pump, shipping surcharges on imports, or the cost of electricity where gas supplies get interrupted.

Under stressful scenarios, banks react too. Lenders tighten credit for shipping and commodity trading firms that face bigger counterparty and freight risks. Credit lines get reviewed. Letters of credit change terms. Those are less visible in headlines but they affect working capital for companies that physically move goods.

Markets dislike uncertainty; calming them usually requires getting ships moving reliably again, which pushes insurance costs down. That's where diplomacy and power politics intersect with finance.

Where China fits — and why its role matters to markets

Point is, who can influence Tehran or Moscow matters to traders. China is a big economic player with deep trade ties across the region. If Beijing used its leverage to press for de‑escalation, that would matter — not because one government sent a memo, but because commercial flows would become easier to insure and price.

Markets won't treat Beijing like a miracle cure — traders assign odds to diplomatic moves and price assets based on those odds. If diplomatic pressure looks like it will lower the odds of a prolonged blockade or a broader supply shock, risk premia fall. If not, they stay elevated. The mechanism is predictable even if the outcome isn't.

At the same time, China is a major consumer and trader in energy markets. Any diplomatic move that affects crude flows through the Gulf or changes sanctions enforcement could re-route trade and shift the demand-supply balance. Traders will model those outcomes quickly. Freight rates and commodity hedges tend to move first; equities and long-term investment decisions move after.

Why Spain's voice would matter for finance

Spain lacks the military clout of the U.S., but its public pressure can still amplify diplomatic messages from Europe and shift perceptions in some markets. If Madrid publicly urged Beijing to do more to reduce hostilities, it would be trying to change political probabilities. That in turn would change market probabilities.

Stocks tied to shipping, energy producers, and insurers are the most sensitive. Banks and trading houses that hold open positions in commodity derivatives are next. And consumers feel the tail end of all that through higher import prices or elevated energy bills. The chain is short and painful when supply is tight.

That said, not every diplomatic appeal moves markets. Traders look for leverage: what can the diplomatic actor actually deliver? What can the counterparty actually change? And how credible is any proposed de‑escalation? Those questions are the ones that drive price moves more than the rhetoric itself.

What to watch on the calendar

Folks watching markets should track a few concrete items. One: any operational announcements from militaries or port authorities about closures or blockades. Those create immediate supply shocks. Two: industry indicators — freight rates, ship insurance premiums, and futures curves for key commodities. Three: statements from major trade partners or guarantors of navigation rights — those shift perceived risk.

Right now, Al Jazeera reported the U.S. Military's posture around Iranian ports and the Strait of Hormuz. That's a clear operational development. At the same time, the BBC has highlighted the human toll inside Ukraine, which signals ongoing damage to local energy infrastructure and the longer-term costs of reconstruction — costs that European governments and markets will have to underwrite over time.

Investor playbook — short-term and structural steps

In the short run traders should hedge energy bets, watch futures curves for contango or backwardation, and track freight‑rate swaps if they book physical voyages. For corporate treasurers, it means stress testing supply chains and securing alternative routes or buffer inventories.

Long-term investors should stress-test supply scenarios and factor higher reconstruction costs into European energy and infrastructure forecasts.he story is about reallocation. Chronic geopolitical risk incentivizes investment in diversified supply chains and in technologies that lower dependency on vulnerable routes — think more local storage, more flexible procurement, and more resilient contracts. Those moves are slow, but they change balance sheets over years, not weeks.

And for insurers and banks, re-underwriting war and transit risk is the immediate work. Premiums rise when risk is higher. That gets passed on to shippers and, eventually, to consumers.

Policy signals matter

Diplomatic signals — from Madrid, Beijing, Washington, or elsewhere — are another input to pricing. They don't always have immediate technical effects, but they shape expectations. Markets price expectations. So when a government signals it plans to press for de‑escalation, the market assigns a probability to that outcome and trades on it.

That makes even seemingly symbolic actions relevant for finance. When humanitarian stories like the BBC's stove deliveries surface, they're reminders that conflict isn't abstract. It destroys infrastructure. It shifts costs. And those are the kinds of costs investors attempt to forecast and absorb.

Related Articles

- Iran urges supporters back to streets as Islamabad talks stall and Washington warns of blockade

- How Washington Could Turn a Fragile Ceasefire Into a Lasting Peace

- Talks Collapse Between Washington and Tehran After High-Level Meetings

U.S. Central Command said vessels will still be able to transit the Strait of Hormuz to and from non‑Iranian ports.