Expect tax payments in mid‑April to move money into the Treasury’s account and temporarily reduce cash in the broader funding market, which already looks stretched. Look, the cash cushion has already stopped growing. But markets that seem calm right now may be misreading what those mechanical flows are hiding — the underlying liquidity picture is weaker than it looks.

Why April matters to funding

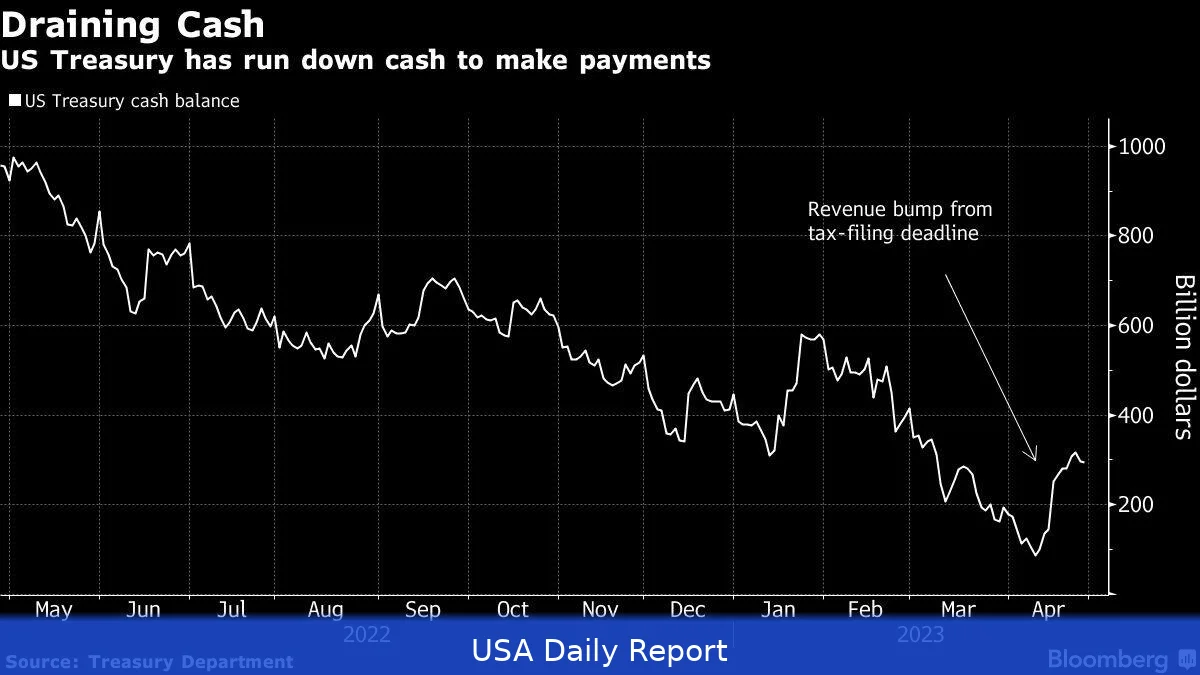

Tax receipts in mid-April tend to move a lot of money into the Treasury’s account at the Federal Reserve. That puts cash into government hands — and temporarily out of the short-term funding system banks, money funds and dealers rely on. In 2025 the macro picture changed when Treasury’s cash balance peaked and then began a steady drawdown, according to the April Macro Liquidity Report. The report warned that with the debt ceiling limiting new borrowing, Treasury would have less flexibility to replace that cash once it leaves the system.

That dynamic matters because the Treasury General Account, or TGA, acts like a tap. When it swells, liquidity across the market can tighten as cash moves to the government. When it falls, liquidity loosens — if Treasury replaces funds by issuing short-term paper or borrowing more. But right now that replacement option is restricted by the legal cap on new debt.

Temporary plumbing is hiding the problem

Markets have seen some relief from scheduled T-bill paydowns. Those paydowns return cash into the system for a short time, creating the sense that liquidity is fine. But those inflows are mechanical and limited. Those technical inflows don't alter the core fact: the TGA has started falling, and fiscal deficits mean Treasury will need to issue more paper once the ceiling is lifted.

Rallies in both bonds and stocks over recent weeks looked like they were supported by easier financial conditions. The Macro Liquidity Report argued those rallies are partly built on a misread — traders are mistaking temporary technical flows for durable liquidity. So prices can flip quickly when issuance resumes in earnest.

What happens when the ceiling lifts

When the debt limit is removed, Treasury will have two main tasks: rebuild its cash buffer and fund ongoing deficits. When the limit goes, Treasury will likely sharply ramp up bill and coupon sales to rebuild balances and cover deficits — not ease into it. The report describes that shift as immediate and severe — not gradual.

Dealers, money funds and foreign investors will face a supply wave with little ramp to absorb it.

And absorption could be tricky. The market has had weeks of orderly rate structures. But the report warns those structures can be upended by a single trigger — a surge in bill and coupon supply that forces trading desks to reprice quickly. That recalibration could be mechanical at first — forced sales, wider bid-ask spreads — and then broader, as duration and intermediation costs rise.

Funding strains beyond the TGA

Think of the funding system as a set of interlocking markets: repo desks that borrow and lend secured cash, money funds that provide short-term liquidity, dealers that warehouse issuance, and overseas buyers who take paper for yield. The report lays out pressure points across funding, absorption and foreign capital behavior. All those levers are in motion already — and some are sensitive to timing and scale.

If dealers have to absorb a larger slice of supply than they expected, they may turn to secured funding markets more aggressively. That pushes up short-term rates. And those rate moves ripple into longer maturities when investors demand higher compensation for holding duration. What seems orderly now can look very different once Treasury sits down to rebuild balances.

Why technical flows confuse price signals

There are two kinds of flows right now: mechanical and discretionary. Mechanical flows are things like scheduled bill redemptions or coupon payments that return cash to the market on a set timetable. Discretionary flows come from investors actively buying or selling based on valuation or need. The mechanical flows can mask declining discretionary liquidity — giving a false sense of calm.

That matters because market participants price risk off what they see in the moment. If dealers and asset managers treat mechanical returns as durable, they may underprice the risk that supply resumes. The report argues the result is a fragile calm — markets look orderly, but they're vulnerable to a rapid repricing once issuance changes.

How participants should be thinking

Look, The main point for funding desks and portfolio managers is to stress-test balance-sheet plans against a sudden jump in supply. The report suggests running scenarios where Treasury rebuilds either a minimal buffer or a more generous one — both scenarios push a lot more paper into an already stretched market. That sort of exercise forces firms to think about where they would get cash, how much they could warehouse, and whether client flows could turn adverse.

Point is, complacency can be costly. If dealers and funds assume current conditions will persist because of short-lived technical inflows, they risk being squeezed when the funding curve reprices. That can show up as higher repo rates, wider money-fund spreads, or faster selling in the bill market.

What to watch next

Monitor the TGA closely. Its trend gave the first warning signs — peaking and then sliding. Keep an eye on issuance calendars and dealer positioning. Also watch foreign demand: if overseas buyers pull back when supply surges, the burden falls more heavily on U.S.-based market makers.

And don't ignore the timing of mechanical flows. T-bill paydowns can create false comfort; they won't make up for large deficit-driven issuance once the ceiling is lifted. That's when the market will find out how much slack remains in funding channels.

Reality check: a single big supply shock can flip orderliness into disorder quickly — dealers and funds should plan for that possibility now.

Bottom line for investors and policymakers

For investors, the immediate implication is to reassess short-term funding risk and liquidity buffers. For policymakers, the lesson is about sequencing and transparency — how Treasury decides to rebuild balances affects market functioning. The Macro Liquidity Report framed the current phase as deceptive: temporary technical supports are masking a one-way drain that becomes pronounced once borrowing resumes.

So expect a pronounced shift in issuance once constraints ease. That will test dealers' capacity, money funds' resilience and the price discovery process across short-term rates and the belly of the curve. The stakes are in how quickly markets can reabsorb issuance without forcing fire sales or abrupt repricing.

Related Articles

- Wall Street Shrugs Off War-Driven Volatility

- JPMorgan tops Q1 estimates, profit rises to $16.49B

- Central Banks Face Rising Inflation Expectations

The April Macro Liquidity Report says Treasury’s cash balance had peaked and the drawdown had begun.