Beijing cut exports of dual-use goods to Japan this month. The move is raising alarms in trade and finance circles.

Beijing's new lever

On January 6, 2026, the Ministry of Commerce announced an immediate ban on certain dual-use items, including some rare earth elements, bound for Japan. That prohibition is designed to stop technologies and materials that can be used for both civilian and military purposes from crossing the border. The decision followed a series of political frictions between Tokyo and Beijing and landed squarely on companies that operate across both markets.

This move goes beyond a simple trade adjustment. China is clearly using export rules strategically to respond to political statements and security shifts.

The Ministry of Commerce framed the move as a national-security screening measure, but its timing after comments by Japanese Prime Minister Takaichi Sanae in November 2025 — in which she suggested a Chinese attack on Taiwan might threaten Japan's survival — makes the economic signal plain. Japan and China are deeply intertwined commercially: China remains Japan's largest trading partner and holds a commanding position in key segments of the supply chain, especially certain rare earths and processing capacity.

China has used export pressure before. In 2010, Beijing halted rare-earth shipments to Japan for about two months amid a territorial dispute. That episode is part of the backdrop now — and officials in Tokyo warned the new restrictions could shave hundreds of billions of yen from growth if extended.

Washington's counterpunch and the widening arms race

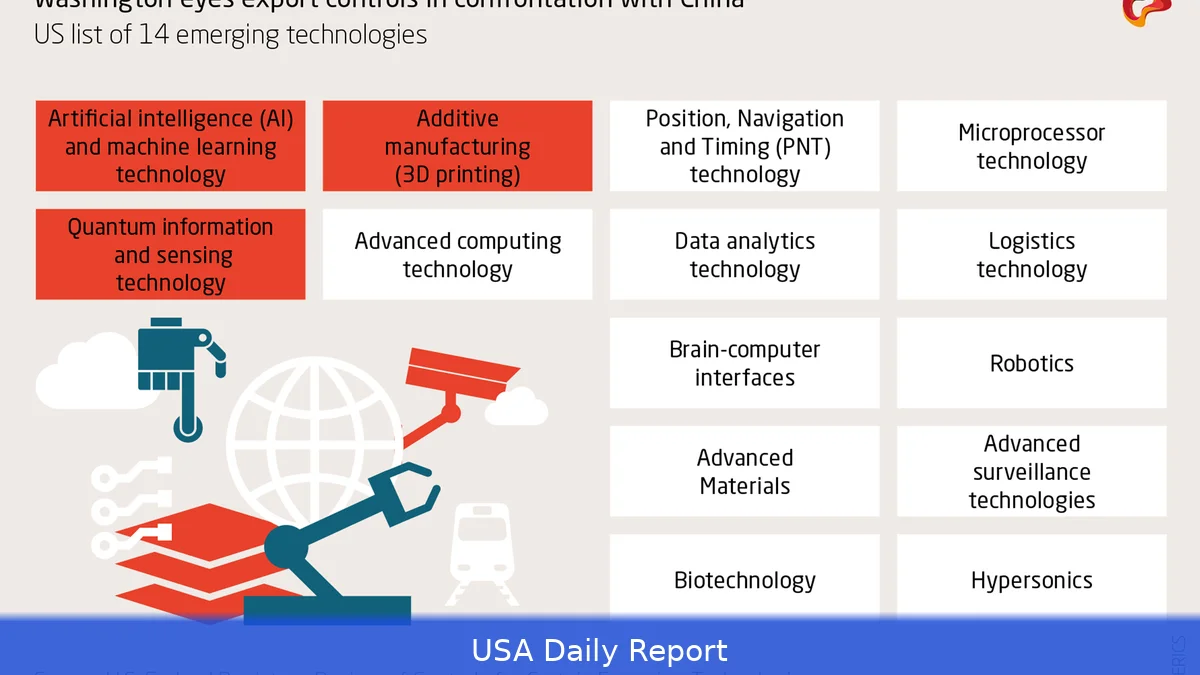

U.S. Policymakers have been reshaping export controls too. The Department of Commerce, via the Bureau of Industry and Security, used authority granted under the Export Control Reform Act of 2018 to curb exports of advanced semiconductors, high-performance computing chips and related equipment to China beginning in October 2022. The rules have been broadened through 2023 and 2024 to reach foreign-produced items when U.S.

Tech is used in their making — the so-called foreign direct product rules.

The key point is that both countries have expanded their export control measures. Washington says the restrictions are about stopping military uses of cutting-edge tech. Beijing says its measures protect national security and prevent diversion to hostile ends. As a result, export controls have shifted from being multilateral safeguards to unilateral tools of state policy.

Industry felt that shift in concrete ways. The U.S. Efforts reached across borders, prompting other governments to adopt similar measures or to coordinate their own controls. Companies such as Dutch chip-equipment maker ASML found themselves swept into the debate because their gear contains U.S. Components or software — and so regulators claimed jurisdiction. The Dutch government later imposed comparable limits, showing how U.S. Policy can pull partners into tighter belts on critical technology.

For many years, export controls were coordinated through consensus platforms such as the Wassenaar Arrangement. That's changed. Now rules are being used not only to block transfers for national security reasons, but to shape competition with strategic rivals. The result is what analysts call an export-control arms race — each side expanding its reach to protect advantages and to punish adversaries.

Supply chains in the crossfire

Rare earths are an easy example. They aren't rare in geological terms, but China dominates refining and processing. Japanese industry has chipped away at dependence since 2010, and Japan's reliance fell from about 90 percent of its rare-earth supplies in 2010 to roughly 60–70 percent by the mid-2020s after years of diversification. Still, China controls many heavy rare earths like terbium and dysprosium that are hard to replace quickly.

That concentration matters for automakers, electronics firms and defense suppliers. Interruptions reverberate through production lines. When one country controls a choke point, it can throttle output or impose vetting steps that raise costs and slow delivery.

Companies are now dealing with increased complexity. They have to map their inputs more carefully, track where processing occurs, and build contingency stockpiles. Some are relocating parts of their supply chains. Others are investing in recycling and substitution. None of that happens overnight. It costs money, time and market share.

Investors have taken note of these changes. Markets repriced risks for companies with deep exposure to contested inputs or to manufacturing footprints inside rival powers. That shift shows up in equity valuations, bond spreads and M&A decisions — firms with more flexible sourcing or stronger local footprints in like-minded countries tend to command higher premiums.

Geopolitics meets finance

Edward Fishman, author of the book Chokepoints, put the change bluntly: "The global economy was designed for the benign environment of the 1990s when we assumed that China and Russia would be our friends. But we're living in a period of intensifying geopolitical competition." His observation points to a broader lesson: trade integration once lowered costs and smoothed markets. Now it also creates strategic vulnerabilities.

Financial institutions are adapting. Lenders and insurers are updating risk models to factor in trade policy shocks. Export-credit agencies and sovereign funds are rethinking where they place capital. Banks that underwrite trade finance are scrutinizing letters of credit for compliance with new export rules. And asset managers are running scenario tests on supply-chain sanctions and targeted trade bans.

But capital can't be redeployed instantly. Plant builds take years. Rare-earth processing plants need specialized inputs and environmental permits. So even if companies and governments decide to diversify, the transition will be gradual — and markets will price a period of elevated uncertainty.

What this means for businesses and policymakers

Frankly, companies should stop assuming rules stay put. They need real-time compliance systems and geostrategic stress tests, not just cost-cutting playbooks. Boards must ask whether supply chains are resilient enough for a world where export policy is a lever of coercion.

Policymakers face trade-offs. Hardening domestic industries reduces exposure to coercion. But reshoring and protectionism raise costs for consumers and firms, and they can fragment global production. Coordinated multilateral approaches were once a restraint on weaponizing trade. Those forums still matter — but they haven't kept pace with how states now use export controls.

So expect more tactical moves. Tariff and export policy will be part of diplomatic bargaining. Entanglements between national security and commercial policy will grow deeper. That's a shift for financial markets: the risk isn't only demand cycles and inflation. It's rules changing overnight because a foreign ministry or a regulator decides strategic priorities have shifted.

One immediate effect is higher hedging and insurance costs for cross-border trade in sensitive inputs. Another is a premium on suppliers who can certify origin and processing transparently. Both raise prices for end consumers and squeeze margins for manufacturers that can't pass costs along.

Still, there are opportunities. Firms that build transparent, verifiable supply chains and those that invest in alternative processing capacity stand to win. Governments that fund diversification or incentivize substitution can protect domestic manufacturing while creating new export sectors.

Related Articles

- Chinese Rare-Earth Stocks Rally as Markets Price in Tighter Supply and Higher Quotes

- Korean Air Delivers Earnings Surprise, Warns of Rising Fuel Costs

- Taiwan Seen as Key Beneficiary of AI-Driven Chip Spending, Analysts Say

On January 6, 2026, China's Ministry of Commerce announced a ban on certain dual-use exports to Japan, including some rare earth elements.