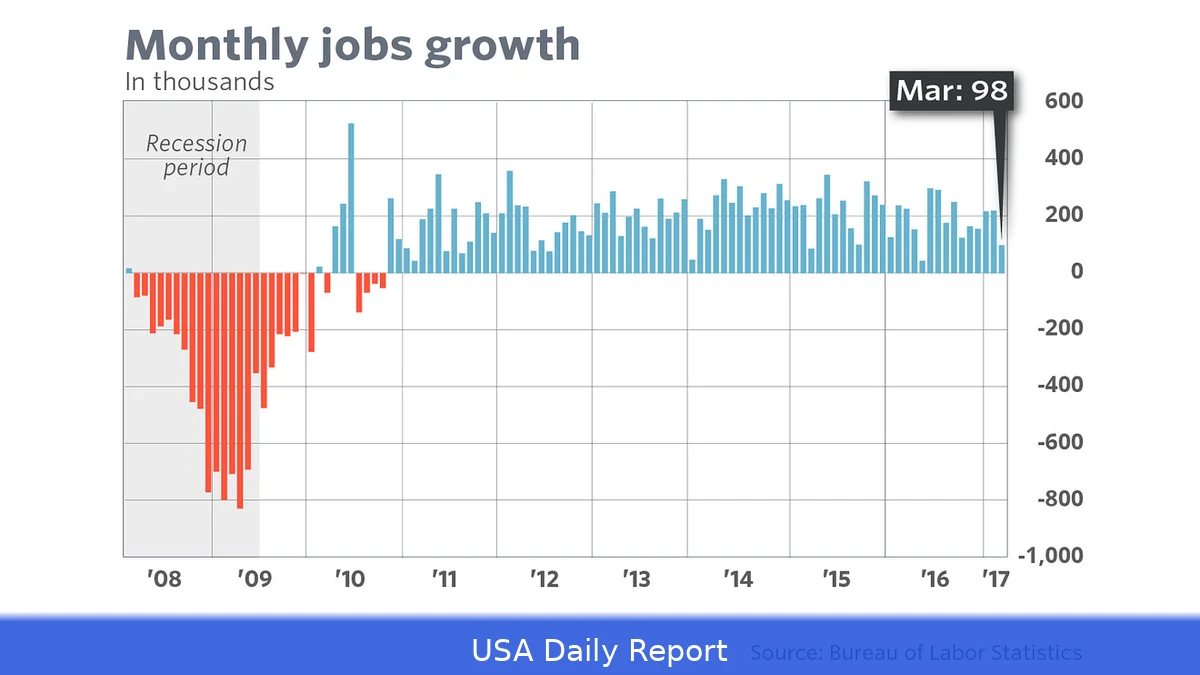

March brought a surprising boost to the U.S. Job market as employers added 178,000 jobs, rebounding sharply from February’s unexpected losses. The unemployment rate also slipped to 4.3%, hinting at resilience amid economic challenges.

Unexpected Job Gains Shake Off February Slump

The Labor Department's latest report revealed a much stronger labor market than economists anticipated. After shedding 133,000 jobs in February, March’s 178,000 new positions marked a strong turnaround, nearly tripling forecasts. The bounce-back was a clear sign that businesses may be regaining confidence despite global and domestic pressures.

Still, the unemployment rate’s drop from 4.4% to 4.3% doesn’t tell the whole story. The labor force—the total number of people working or actively seeking work—shrank by 396,000 in March. That pulled the participation rate down to 61.9%, the lowest since late 2021. Fewer people competing for jobs can mask some underlying weaknesses in the market.

Healthcare and Construction Lead Hiring

Over half the new jobs popped up in health care and social assistance, sectors often linked with the country’s aging population. Healthcare alone added 76,400 positions, buoyed by 31,000 Kaiser Permanente employees returning after a strike ended in February. Construction firms also hired 26,000 workers, likely helped by milder weather that made projects easier to restart.

Manufacturing showed a modest gain of 15,000 jobs, though factories have still lost jobs in 14 of the past 16 months. That points to ongoing struggles in the sector despite some positive signs.

Wage Growth Remains Modest

Average hourly wages inched up 0.2% from February and were 3.5% higher than a year ago. That annual increase is the smallest since mid-2021 and aligns closely with the Federal Reserve’s 2% inflation target. Wage growth slowing to this pace might ease some inflation concerns, but it also reflects cautious employer behavior.

Uncertain Outlook Despite March Strength

Last year saw the weakest job growth outside of a recession since 2002, with employers adding an average of just 9,700 jobs monthly.

Many businesses have stayed wary of hiring new workers, caught between tariffs, immigration policies, and fears over artificial intelligence disrupting entry-level roles.

Economists describe the current environment as a “no-hire, no-fire” market, where companies hold onto current employees but hesitate to expand or cut their workforce significantly. That dynamic creates challenges for younger workers and those entering the job market for the first time.

Global events cloud the horizon, too. The war involving Iran and rising energy prices, which recently pushed U.S. Gas prices above $4 a gallon for the first time since 2022, threaten to impact hiring in coming months. Economists caution that March’s data likely doesn’t fully capture these effects yet.

Diane Swonk, chief economist at KPMG, pointed out that big tax refunds from recent tax cuts are helping support the economy but are being offset by rising energy costs. Thomas Simons, chief U.S. Economist at Jefferies, noted that the numbers are mostly backward-looking and may not reflect these emerging risks.

Federal Reserve and Labor Market Dynamics

Federal Reserve Chair Jerome Powell recently commented on the labor market’s flat private sector job creation, saying it matches the very slow growth in the labor force itself. High interest rates and policy uncertainties are making businesses cautious. Yet, firms seem reluctant to lay off workers, creating a labor market stuck in place.

That situation might keep unemployment stable for now but could mean slower economic growth ahead if companies don’t feel confident boosting hiring. The mix of solid March job gains with subdued wage growth and shrinking labor force participation paints a complex picture.

March’s jobs report shows a U.S. Labor market trying to bounce back, but it’s far from clear if the momentum can hold as global tensions and economic pressures mount.