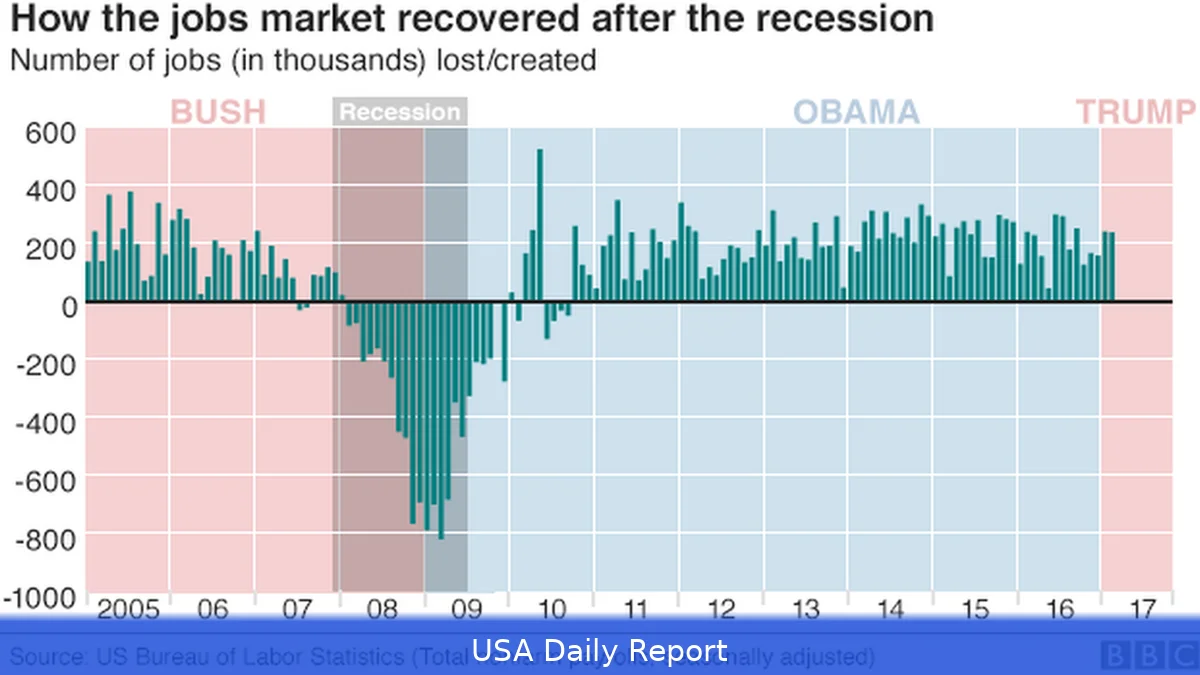

March brought a rebound in US hiring following a steep drop in February, with 60,000 new jobs reportedly added. The labor market is a bit shaky but holding steady, even as inflation worries and global tensions continue.

Labor Market Volatility Continues

The US job market took a hit in February, shedding 92,000 jobs—a rare decline since the pandemic began. But March appears to have reversed that trend, with economists forecasting 60,000 new positions added. These estimates come from a Bloomberg survey ahead of the monthly employment report due Friday.

Payrolls haven’t increased two months in a row since last May. That points to limited momentum in hiring, with neither a surge nor a sharp drop in available jobs. The unemployment rate will probably hold steady at 4.4%, reflecting a balance between job seekers and openings.

Sector-Specific Shifts and External Pressures

The February drop likely stemmed from weather-related disruptions hitting construction and the leisure and hospitality sectors hard. March should show a reversal, with those industries recovering. Health care jobs may also help the numbers, thanks to the end of a strike involving over 30,000 Kaiser Permanente employees.

However, seasonal changes aren’t the only factors affecting the market. The war in West Asia has pushed up gasoline prices, rekindling inflation worries among Americans. That’s putting pressure on consumer spending, even as retail sales data for February suggest demand held up, buoyed by a rebound in car purchases. Excluding volatile sectors like auto dealers and gas stations, economists expect retail sales to grow by 0.3%.

Fed’s Balancing Act Amid Inflation and Hiring

Fed officials are keeping a close eye on these conflicting signs. On one side, hiring remains sluggish and consumer demand shows signs of strain. On the other, energy price spikes risk driving inflation higher.

Fed Chair Jerome Powell is set to discuss these challenges at Harvard University on Monday, potentially offering insights into how the central bank views the risks to inflation and employment.

Bloomberg Economics analysts anticipate March nonfarm payroll growth of roughly 80,000 jobs, factoring in the boost from returning strike-affected workers and continued weakness in private-sector hiring. They expect the unemployment rate to stay put, aligning with current labor force trends.

Wider Economic Indicators and International Context

Other economic data this week could shed more light on the economy’s direction. The Institute for Supply Management is likely to report a third consecutive month of growth in manufacturing activity for March—a sign of potential stabilization after a shaky 2022.

North of the border, Canada’s GDP figures for January and February point to tepid growth. The Bank of Canada recently held interest rates steady, a decision that might be better understood once policymakers’ deliberations are released. Trade data for February will probably confirm ongoing deficits amid tense US trade relations.

On the global stage, Group of Seven energy and finance ministers are scheduled for a virtual meeting Monday. Countries across the eurozone and Asia are monitoring energy markets closely, influenced by geopolitical uncertainties that also affect inflation and growth prospects worldwide.

The March jobs report should show if the US labor market can keep improving or if the ups and downs will continue. Fed policymakers and investors alike will be watching closely as inflation pressures and geopolitical risks continue to shape the economic outlook.