Japan's 10-year government bond yield jumped to about 2.43% on Monday. Markets are recalibrating fast.

Yield spike and immediate drivers

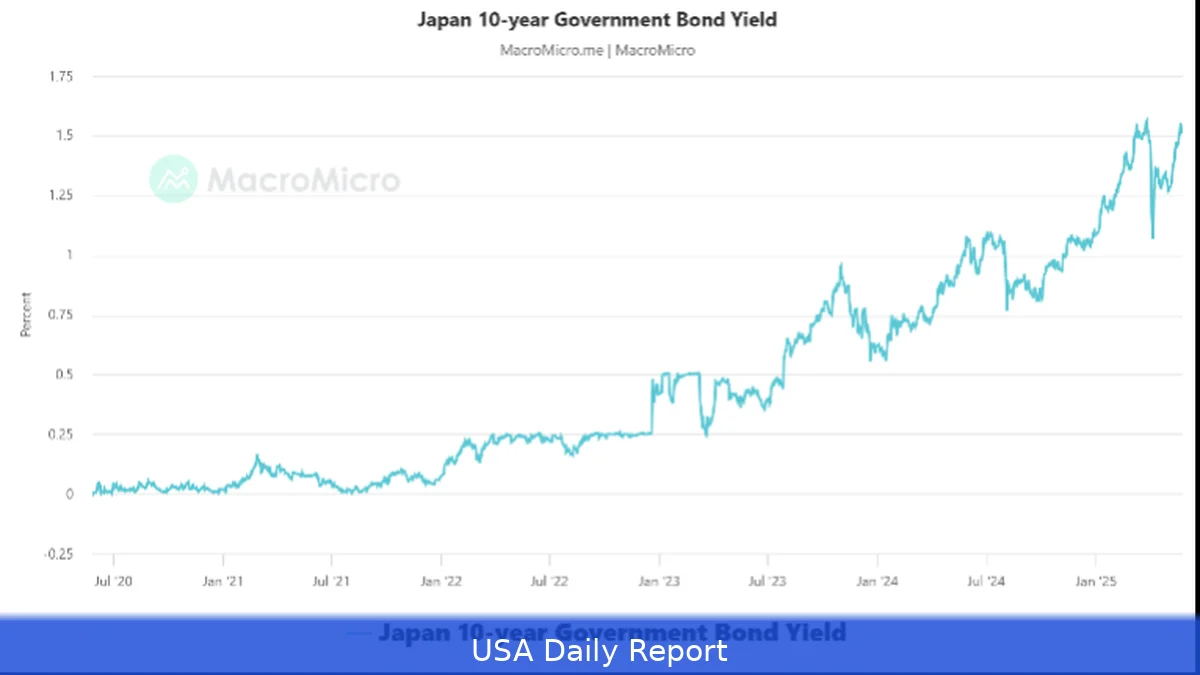

Japan's 10-year government bond yield rose to roughly 2.432% on Monday, the strongest level seen since July 1997. Look, that's a dramatic change from the near-zero rates that had defined Japanese fixed income for much of the past decade. The move comes as inflation in Japan's overall economy has picked up, and the yen has weakened to about 160 per dollar, adding pressure on prices and on policymakers.

Short paragraph for punch.

Why yields are climbing

First, inflation is trending higher than it has in years. Japan's GDP deflator, which measures inflation across the whole economy rather than just consumer prices, rose 3.4% year-over-year in the fourth quarter. That's close to U.S. Overall inflation in that quarter, which ran at about 3.8%.

Second, energy costs have surged after the conflict in Iran pushed crude prices up. The higher oil bill feeds into domestic prices and forces investors to demand more compensation for future inflation.

Japan's Finance Ministry explicitly cited the oil shock when it raised the coupon on new 10-year bonds.

Third, the Bank of Japan has stepped back from the aggressive bond buying that kept yields artificially low. The BOJ stopped increasing its JGB holdings at the end of 2023 and began shrinking its balance sheet in 2024. As of the quarter ending Dec. 31, the BOJ's total assets were down about 10.4% and its holdings of Japanese government bonds fell about 8.1%.

Coupon reset and the government's math

Japan's Finance Ministry raised the coupon on newly issued 10-year bonds to 2.4%, up 0.3 percentage points from March, the ministry said. That's the highest coupon for new 10-year paper since July 1997.

Thing is, the extra interest the government promises now has a cost. The ministry has set aside a record 13 trillion yen—around $81 billion—for interest payments on government debt in the fiscal 2026 budget, and it did that assuming a long-term interest rate of 3.0%. If market rates stay below that assumption, the budget projection holds; if they rise, the government's interest bill may climb further.

Debt load, ratings and investor appetite

Japan carries one of the largest debt burdens among developed economies, and credit ratings reflect that. Fitch assigns Japan an 'A' rating, while S&P rates the country 'A+' and Moody's 'A1'. Those grades sit several notches below the top 'AAA' level.

Higher yields make new bond issuance easier to sell, on paper. But the numbers on the table show Not just about offering a better coupon. Investors also see a mix of fiscal strain and still-heavy state-linked ownership. The BOJ alone holds roughly half of all outstanding JGBs, and other government-linked entities—like Japan Post Holdings, which partly remains state-owned—own sizable chunks too. That concentration changes the market's liquidity and who actually sets prices.

Longer maturities and recent swings

Sure, longer-term JGBs have climbed even more. The 30-year yield jumped about 8 basis points to 3.76% on the same day and has traded at record levels for that bond since its introduction in 1999. In mid-January, the 30-year yield spiked nearly 42 basis points after then-new Prime Minister Sanae Takaichi floated plans for bigger government spending alongside tax cuts—a combination that would increase issuance.

Authorities tried to calm markets after those moves. Yields fell more than 60 basis points by late February, but they've been creeping higher again since then.

Bank of Japan: from buyer of last resort to a smaller role

The Bank of Japan's reduction in bond purchases represents a strategic shift. For years, quantitative easing and yield-curve control kept interest rates pinned near zero. The BOJ's decision to halt increases in its JGB holdings at the end of 2023 and then begin quantitative tightening in 2024 has removed a structural buyer that many investors assumed would always be there.

And when a giant buyer steps back, markets have to find new marginal buyers—pension funds, insurers, foreign investors. That can push yields higher during periods of heavy issuance or rising inflation expectations.

Global spillovers and what investors face

Japan's rising yields aren't contained. There were moments earlier this year when moves in JGB yields showed up in U.S. Treasury markets, prompting commentary from foreign officials and market participants. Higher yields in Japan can reprice risk-free curves elsewhere, at least for short stretches.

For international investors, Japan now offers higher nominal returns than it did a few years ago, but the returns come with different trade-offs: a weaker yen, higher inflation, and a large government funding program that will likely keep issuance elevated. That's a package some buyers will take, others will avoid.

What the market is watching next

Investors will be watching supply plans closely.

The government's fiscal math assumes long-term rates near 3.0% and includes record interest-payment allocations. If the market's asked yield stays below that level, bond sales will be easier. If rates drift above it, the fiscal strain will grow.

Policy signals from the Bank of Japan matter too. The BOJ has already pared back asset holdings, and further normalization—if it happens—will keep upward pressure on yields. But the central bank still holds an enormous share of the market, and any sizable change in its posture would be a major market event.

One more thing: the yen's slide toward 160 per dollar amplifies the story. A weak currency raises import costs and can force the BOJ to act sooner than officials might otherwise prefer—especially if oil and commodity prices remain elevated.

Short paragraph to break the rhythm.

Investor takeaways

For bond investors, the era of near-zero Japanese yields looks to be receding. Yields are higher and more volatile. For global portfolio managers, Japan now offers yields that are competitive on paper, but currency risk and domestic fiscal dynamics make the picture.

For Tokyo, the balancing act is clear: finance a large public debt pile while keeping borrowing costs manageable. Higher coupons help sell bonds today. But they add to the bill tomorrow.

Related Articles

- Why water bonds could unlock fresh funding for African infrastructure

- CapitaLand Raises $320 Million for New Asia-Pacific Credit Fund

- The ‘Annoyance Economy’ Is Quietly Costing Americans Hundreds of Billions

The Finance Ministry raised the coupon on new 10-year bonds to 2.4%, the highest since July 1997.