Markets now price a June ECB rate hike. Traders and banks point to rising energy costs and fresh inflation signals.

Market odds tilt toward June

Financial markets are lining up behind a June interest-rate increase by the European Central Bank after pricing in a pause at the late-April meeting. Data from LSEG show traders expect policymakers to hold at the April 29-30 decision and to deliver tightening at the next meeting in June. Many market participants now foresee the ECB’s key rate reaching at least 2.5% by year-end — a rise of roughly 50 basis points or more from where rates stood earlier this year.

Volatile energy prices and tensions in the Middle East have pushed market odds in this direction. Prediction-market indicators and brokerage forecasts have moved in the same direction, lifting the perceived probability of a near-term move by the central bank.

Investors now see clearer pricing signals. Short-term money markets have pushed up expected path-of-rates curves, and fixed-income traders are now hedging for additional tightening later in the summer and into the autumn.

J.P. Morgan revises its calendar

J.P. Morgan economists have adjusted their timetable for policy moves. The bank now projects two quarter-point hikes, in June and again in September 2026, replacing earlier calls for an April and a July increase.

Major brokerages are also shifting toward expecting a slower tightening later this year.

The bank cites stronger-than-expected energy prices and the risk of inflation spillovers as the main drivers behind its new forecast. A persistent rise in energy costs would feed into headline inflation and could keep core inflation pressures elevated, the economists argue. That, in turn, would limit the ECB’s room to delay further action.

J.P. Morgan’s call also reflects the view that the central bank is unlikely to deliver large, front-loaded moves. The bank’s scenario points to measured, stepwise increases rather than an aggressive emergency-style lift.

Energy and geopolitics in focus

Oil and gas markets are now a critical input for monetary policy decisions. Traders on prediction venues and commercial desks have been pricing the chance of crude climbing toward $90 a barrel in the weeks ahead, a move that would add upward pressure to euro-area inflation.

Policymakers have warned that supply disruptions or production cuts might raise energy prices. That risk is elevated by uncertainty around the Strait of Hormuz and ongoing tensions involving Iran, which central bankers say could create fresh shocks to the global energy complex.

In public remarks at the IMF Spring Meetings in Washington, D.C., Joachim Nagel, president of Germany’s Bundesbank, warned that recent oil-price moves had left the outlook sitting "between our baseline and our adverse scenario." He said developments in the region were feeding daily news and data that policymakers must weigh when they meet.

ECB officials stress meeting-by-meeting approach

Governing Council members have emphasized a cautious, data-dependent strategy. Martins Kazaks, Latvia’s representative on the ECB Governing Council, said the bank is taking decisions one meeting at a time as new information arrives. That approach keeps the policy committee flexible and able to respond to sudden shocks.

Officials keep an eye on headline inflation and core measures that exclude volatile items like energy and food. Minutes and speeches from the ECB’s senior staff indicate they’re particularly alert to any signs that energy-driven price rises are spilling over into wages and services prices — the kind of broadening that would force a firmer policy reaction.

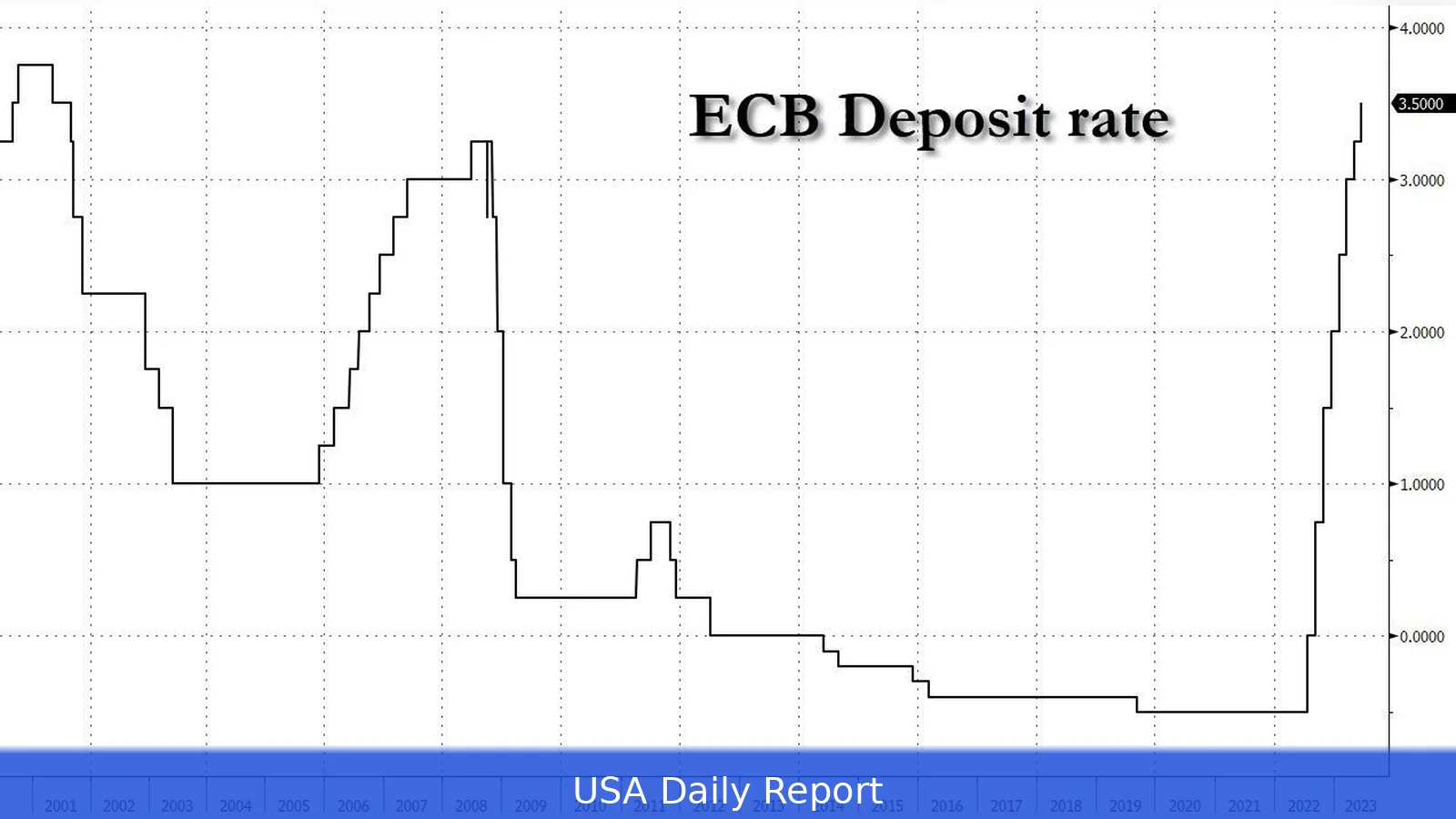

The central bank’s deposit rate was 2% as of March 19, 2026. Against that baseline, markets and banks are now mapping out the path to what they see as a higher terminal rate later in the year if inflation readings keep surprising to the upside.

What the numbers mean for markets and borrowers

For bond markets, an expectation of June tightening has pushed up yields on euro-area sovereign debt across maturities. Shorter-dated yields have reacted most strongly, reflecting the increased odds of a policy move this summer. A higher-for-longer rates outlook also supports the euro versus major peers, at least soon.

Corporate borrowers face a mixed picture. Companies rolling short-term funding will likely encounter steeper borrowing costs, while firms with longer-dated, fixed-rate debt will have shielded themselves from immediate moves. Banks’ lending standards could tighten if rates climb further, raising borrowing costs for households and smaller businesses.

Consumers feel the impact more slowly, but it’s still significant. Mortgage rates in markets with variable pricing or frequent repricing dates will likely tick higher as banks pass on increased funding costs. That could damp household spending and cool demand — a key channel the ECB watches when setting policy.

Signals to watch before June

There aren’t many chances for big surprises before the June meeting. Inflation prints for March and April will be closely read. So will indicators of wage momentum and services-sector inflation, which are harder to reverse once they gain traction.

Energy news is another live input. Any announcement of OPEC+ production cuts or a spike in geopolitical risk could materially alter the policy calculus. Traders are already booking positions to reflect that sensitivity, which explains the recent uptick in pricing for near-term tightening.

ECB President Christine Lagarde’s public remarks in the weeks ahead could also shift market odds. Analysts note that clear language from the president on how the Governing Council interprets recent data would move trader expectations and asset prices.

Why the ECB may still hesitate

Despite the growing consensus for June, the Governing Council faces trade-offs. Rapid tightening can damp inflation, but it can also slow growth and lift unemployment. The ECB has signaled that it wants to balance the risk of inflation becoming entrenched with the danger of over-tightening and tipping the economy into a sharper slowdown.

Officials have highlighted the "meeting-to-meeting" framework as the tool for striking that balance. That posture lets them react if incoming data weaken or if upside inflation surprises persist.

The policy debate will revolve around whether recent price shocks are temporary pass-throughs or the start of a more sustained climb in underlying inflation. If staff projections show that higher energy costs are feeding through to durable price-setting behavior, the case for June action will be stronger.

Markets, meanwhile, are doing their part: when odds change, prices follow. Traders have already moved to price a scenario in which the ECB lifts rates this summer. That mechanical adjustment in turn affects borrowing costs and financial conditions, which the bank will have to factor into its next policy decision.

Related Articles

- Stock Rally Pauses as Traders Eye Iran Ceasefire Outcome

- Treasurer warns inflation could top 5%

- Markets Ignore Weak Economy as War Lingers

"In two weeks, we have to decide what's coming next," said Joachim Nagel, president of Germany's Bundesbank.